Being self-employed offers freedom and flexibility, but it also means you’re fully responsible for your retirement savings. Unlike traditional employees with employer-sponsored plans, self-employed individuals must navigate their own retirement planning. The good news is that several powerful, tax-advantaged options exist in 2026 to help you build a substantial nest egg.

👉💼 Maximize your retirement savings with smart plans designed for self-employed professionals.

This comprehensive guide explores the best retirement plans for self-employed people, current contribution limits, tax benefits, and strategies to maximize your savings while protecting your future.

Why Retirement Planning Is Critical for the Self-Employed?

Self-employed professionals (freelancers, consultants, solopreneurs, and small business owners) often face inconsistent income, higher self-employment taxes (15.3% for Social Security and Medicare), and no employer matching contributions. Proper planning can significantly reduce your tax burden today while securing comfortable retirement income later.

In 2026, with inflation adjustments and updated IRS limits, self-employed individuals have more opportunities than ever to save aggressively.

👉🚀 Build a secure financial future with tax-advantaged retirement planning tools.

Top Retirement Plans for Self-Employed Individuals in 2026

Here are the most popular and effective options:

1. Solo 401(k) – Best for High Earners

Also known as a One-Participant 401(k) or Individual 401(k), this plan is ideal for businesses with no full-time employees other than yourself or your spouse.

👉📊 Explore powerful retirement planning tools designed for self-employed success.

2026 Contribution Limits:

- Employee deferral: Up to $24,500 (pre-tax or Roth)

- Employer profit-sharing: Up to 25% of compensation

- Total combined limit: $72,000 (under age 50)

- Catch-up contributions: $8,000 (age 50–59 or 64+); $11,250 (age 60–63)

The Solo 401(k) offers high contribution potential, Roth options, and loan provisions. It’s one of the most flexible plans for maximizing savings.

2. SEP IRA – Simplest Option with High Limits

The Simplified Employee Pension (SEP) IRA is easy to set up and administer. It’s perfect for those who want flexibility in contributions year to year.

2026 Limits: Up to 25% of net self-employment income, with a maximum of $72,000. Contributions are tax-deductible, and the plan has minimal paperwork.

Note: If you have employees, you must contribute the same percentage to their accounts.

3. SIMPLE IRA – Good for Growing Businesses

The Savings Incentive Match Plan for Employees (SIMPLE) IRA suits businesses with fewer than 100 employees.

👉💰 Plan, calculate, and grow your retirement savings with confidence.

2026 Limits:

- Employee deferral: Up to $17,000

- Catch-up: Additional $3,500 (age 50+)

- Employer must either match up to 3% or contribute 2% of compensation

4. Traditional and Roth IRAs

These serve as supplemental or starter options.

2026 Limits: $7,500 + $1,100 catch-up (age 50+), for a total of $8,600.

Roth IRAs are excellent for tax-free growth and withdrawals if you expect to be in a higher tax bracket in retirement.

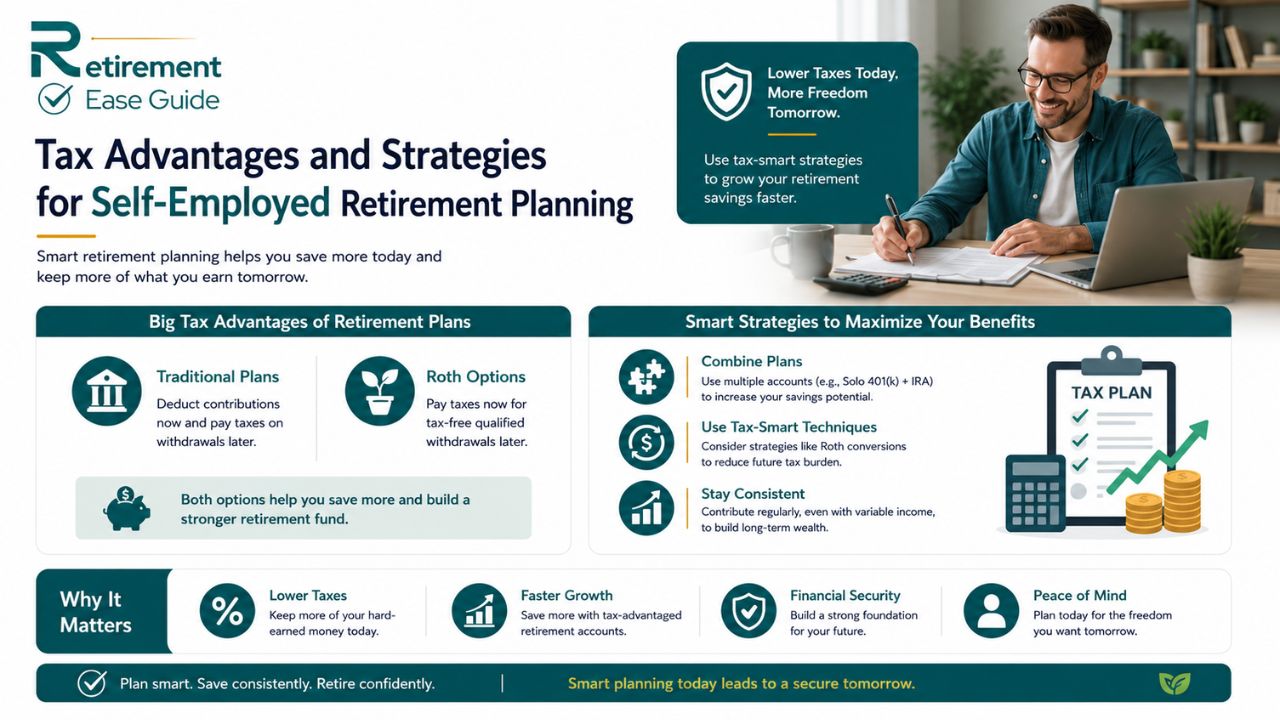

Tax Advantages and Strategies for Self-Employed Retirement Planning

All these plans offer significant tax benefits:

- Traditional plans — Deduct contributions now and pay taxes on withdrawals later.

- Roth options — Pay taxes now for tax-free qualified withdrawals.

👉📘 Use professional retirement tools to compare plans and maximize savings.

Smart strategies include:

- Combining plans (e.g., Solo 401(k) + IRA) when eligible.

- Using retirement tax planning techniques like Roth conversions.

- Contributing consistently even with variable income.

Protecting Your Retirement with Insurance

Self-employed individuals lack employer-provided benefits, so protecting your savings from unexpected risks is essential.

Healthcare remains one of the biggest concerns. Explore the best affordable health insurance for retirees to understand options before Medicare eligibility.

Long-term care can quickly deplete retirement funds. Learn how much long-term care insurance costs to plan proactively.

Life insurance also plays a vital role in legacy and income protection. Review the 5 best life insurance policies for seniors and compare term vs. whole life insurance for seniors.

Once you reach Medicare age, choosing the right coverage helps preserve your nest egg. Compare Medicare vs. private insurance and Medicare Advantage vs. Medicare Supplement plans.

Many self-employed retirees choose vibrant communities for lifestyle and cost efficiency. Discover the best active adult communities for active adults that align with your vision.

👉🌟 Find the right retirement strategy with our powerful financial planning tools.

Common Mistakes to Avoid

- Waiting until year-end to contribute (missing compound growth).

- Underestimating healthcare and long-term care costs.

- Ignoring required minimum distributions (RMDs) rules.

- Failing to diversify investments within your retirement accounts.

Conclusion

Self-employed individuals have excellent retirement plan options in 2026 that can help you achieve financial independence faster than you might think. Whether you choose a Solo 401(k), SEP IRA, or a combination approach, starting early and contributing consistently makes all the difference.

At Retirement Ease Guide, we provide free tools, expert comparisons, and connections to trusted professionals to support your unique journey. Take the next step today — explore our retirement calculators or reach out to an advisor to build a personalized plan that secures your future.

FAQs About Retirement Plans for Self-Employed People

- What is the best retirement plan for self-employed in 2026?

The Solo 401(k) is often best for high earners due to higher limits and flexibility. SEP IRA is ideal for simplicity.

- Can I contribute to both a Solo 401(k) and an IRA?

Yes, in most cases, though income limits may apply to IRA deductibility.

- How much can I save tax-free as self-employed?

Up to $72,000+ in a Solo 401(k) or SEP IRA, depending on your income and age.

- Do self-employed people get employer matching?

You effectively “match” yourself through employer contributions in Solo 401(k) and SEP plans.

- What happens if I hire employees?

You may need to shift to a different plan or include them, especially with SEP or SIMPLE IRAs.

- Are Roth contributions available in these plans?

Yes, many Solo 401(k) plans offer Roth options for tax-free growth.

- How do I set up a retirement plan for my self-employed business?

Work with a financial advisor, accountant, or reputable custodian (Fidelity, Vanguard, etc.). Deadlines vary by plan type.

- Does retirement planning affect my taxes now?

Yes — contributions can significantly lower your current taxable income and self-employment tax burden.