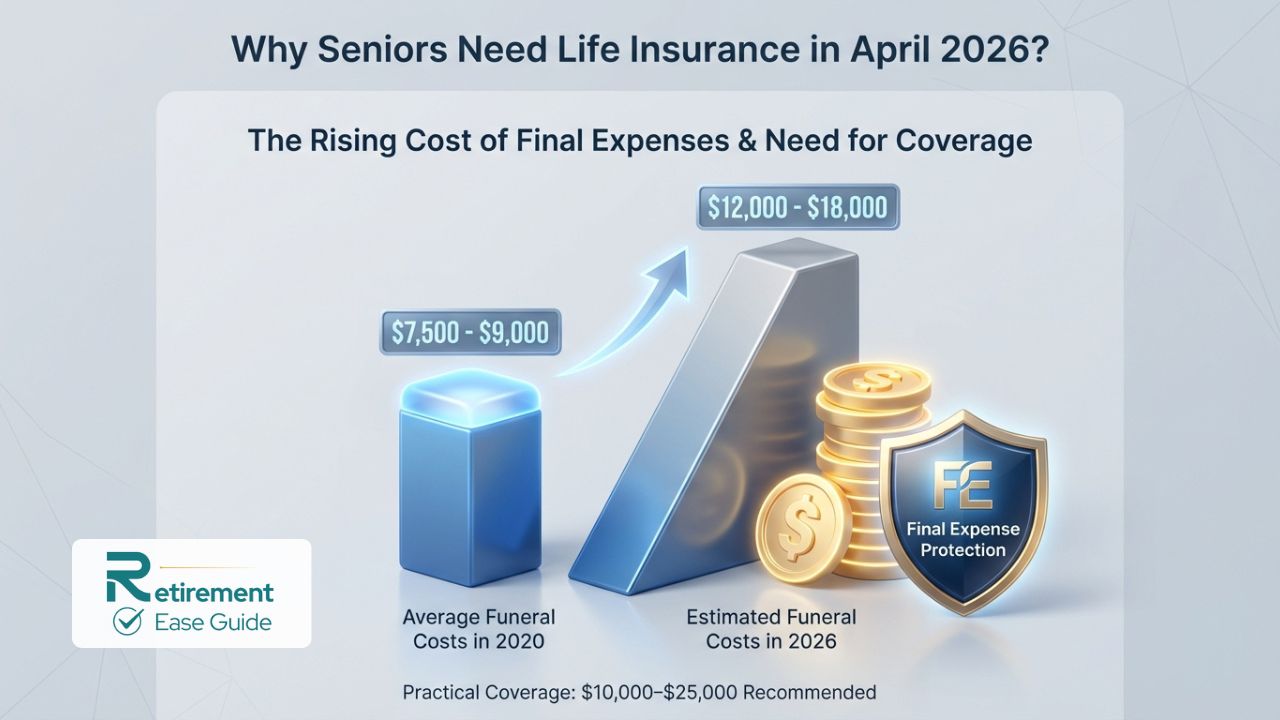

With funeral and end-of-life expenses continuing to rise in 2026, many seniors worry about leaving their families with unexpected financial burdens during an already difficult time. The median cost of a traditional funeral with viewing and burial remains around $8,300 nationally, while adding cemetery fees, a vault, headstone, and other costs can push the total well above $11,000–$13,000. Traditional life insurance can be hard to qualify for due to health conditions common in later years, making specialized senior options essential.

The 5 best life insurance policies for seniors in April 2026 focus on accessibility, affordability, and reliable protection. These include guaranteed issue and final expense (burial) insurance for those with health challenges, no medical exam life insurance for seniors, and value-driven term or whole life options for healthier applicants. With inflation impacting costs and many policies offering fixed premiums that never increase, securing coverage now can bring real peace of mind.

Why Seniors Need Life Insurance in April 2026?

At this stage of life, the purpose of life insurance shifts from income replacement to practical protection:

- Covering final expenses: Funerals, cremation (median ~$6,280), medical bills, outstanding debts, and legal costs can strain family budgets.

- Avoiding burden on loved ones: Without coverage, adult children or spouses may face credit card charges or loans just to handle arrangements.

- Legacy and peace of mind: A modest policy can help with inheritance goals, charitable gifts, or simply easing the emotional and financial transition.

- Inflation protection: Fixed-premium permanent policies lock in today’s rates against future cost increases.

- Supplemental or standalone coverage: Many seniors use these policies where older term life has expired or traditional underwriting is challenging.

Best final expense insurance 2026 and burial insurance for seniors 2026 are particularly valuable because they deliver quick payouts—often within days—to help families focus on grieving rather than finances.

Types of Life Insurance Policies Suitable for Seniors

Seniors benefit from policies designed around their health realities and modest coverage needs.

Guaranteed Issue / Final Expense (Burial) Insurance

These policies guarantee acceptance with no medical exam and no health questions (typically ages 45–85). Coverage is usually $2,000–$30,000. Most include a 2-year graded benefit period: full death benefit for accidental death from day one, but only return of premiums plus interest (often 10–30%) for natural causes in the first two years. Premiums are fixed and higher due to guaranteed issuance. Ideal for those with chronic conditions.

Simplified Issue / No Medical Exam Policies

You answer a few health questions (no physical exam). Approval is fast, with higher coverage possible and often immediate full benefits if approved. These bridge the gap between guaranteed issue and fully underwritten policies.

Whole Life Insurance

Permanent coverage with fixed premiums, lifetime protection (as long as premiums are paid), and potential cash value accumulation. Many senior whole life policies double as top senior whole life policies with living benefits or final expense focus.

Term Life (for Healthier, Younger Seniors)

Lower-cost temporary coverage (10–30 years) available up to certain ages (often 80+). Best for those still supporting dependents or covering specific debts like a mortgage. Convertible to permanent in many cases.

Universal Life Options

Flexible permanent coverage with adjustable premiums and death benefits. Some offer indexed or guaranteed universal life for growth potential or predictability, though these are more common among healthier seniors seeking higher amounts.

The 5 Best Life Insurance Policies for Seniors in April 2026

Based on April 2026 reviews from sources like Forbes, CNBC, MoneyGeek, and U.S. News, here are standout options. “Best” depends on your health, budget, and needs—always verify with personalized quotes.

1. Mutual of Omaha Living Promise / Guaranteed Issue Whole Life

Best for: Guaranteed acceptance and final expense / burial insurance needs.

Key features: Issue ages 45–85 (50–75 in NY); coverage $2,000–$25,000 (higher in some day-one options); no medical exam or health questions; fixed premiums; quick claims process.

Sample monthly premiums (approximate, non-tobacco, $10,000 coverage): Age 65 female ~$22–$42; male ~$29–$54. Age 75 female ~$37–$72; male ~$50–$97. Graded benefit in guaranteed version.

Pros: High issue ages, nationwide availability, strong reputation for accessibility and customer service; A+ financial strength.

Cons: Modest maximum coverage; 2-year graded period in guaranteed issue. Excellent for no medical exam life insurance seniors 2026.

2. Pacific Life Term Life (PL Promise Term or Pacific Elite Term)

Best for: Affordable, higher-coverage term protection for healthier seniors.

Key features: Competitive rates; terms of 10–30 years; coverage starting at $50,000+ (higher minimums for some products); convertible options; accelerated death benefits available. Renewable or convertible in many cases up to advanced ages.

Sample rates: Often among the lowest for term in senior evaluations; exact premiums vary significantly by health and amount—healthier applicants in their 60s can see strong value.

Pros: Below-average costs, pricing stability, strong cash value access in permanent lines; highly rated for seniors by Forbes.

Cons: Requires more underwriting for best rates; not ideal for significant health issues. Great for best life insurance for seniors 2026 seeking value and flexibility.

3. AARP Guaranteed Acceptance Life Insurance (underwritten by New York Life)

Best for: Trusted brand with guaranteed acceptance for AARP members.

Key features: Up to $30,000 coverage; no medical exam or health questions; issue ages typically 50–80+; fixed premiums that never increase; 2-year limited benefit period.

Sample monthly premiums: Vary by age/gender/amount—often competitive within guaranteed category (e.g., mid-$20s to $60s range for $10,000–$25,000 at age 65–75, depending on units/membership discounts).

Pros: Backed by New York Life’s financial strength; member perks; simple application.

Cons: Limited to AARP members; capped coverage; graded benefits initially. A reliable choice for guaranteed issue life insurance for seniors.

4. Physicians Mutual / Gerber Life Guaranteed or Simplified Whole Life

Best for: Affordable guaranteed or simplified final expense with straightforward options.

Key features: Guaranteed acceptance options up to age 80–85; coverage $5,000–$30,000 range; no-exam availability; fixed lifetime premiums. Physicians Mutual often praised for guaranteed issue value.

Sample monthly premiums (illustrative $10,000): Age 65 ~$20–$50 range depending on health tier; higher at 75.

Pros: Competitive pricing in guaranteed category; focus on senior needs; quick payouts.

Cons: Modest coverage limits; graded periods apply in guaranteed plans. Strong contender for best final expense insurance 2026 and affordable senior life insurance plans.

5. State Farm Whole Life or Guaranteed Issue Final Expense

Best for: Personalized service through local agents and reliable permanent coverage.

Key features: Whole life with cash value potential; guaranteed issue options for final expenses (ages 45–80 or 50–75); coverage tailored to needs; strong dividends in some permanent lines.

Sample monthly premiums: Competitive agent-quoted rates; guaranteed issue similar to industry averages for $10,000–$15,000.

Pros: Excellent customer service ratings; financial strength; flexible options including limited-pay whole life.

Cons: May involve more interaction for best rates; some guaranteed products have lower caps. Ideal for those valuing agent support in senior life insurance April 2026.

Side-by-Side Comparison Table of the 5 Best Policies

| Carrier / Policy | Best For | Max Coverage (Typical) | Issue Age Range | Sample Premiums Age 65/75 ($10k approx., non-tobacco) | Waiting/Graded Period | Key Benefits |

| Mutual of Omaha Living Promise | Guaranteed acceptance & burial | $25,000+ | 45–85 | $22–$54 / $37–$97 | 2 years (guaranteed) | High issue age, quick claims |

| Pacific Life Term Life | Affordable higher coverage | $250k–$10M+ | Up to 80+ | Varies (competitive for healthy) | None (if approved) | Low term rates, convertibility |

| AARP / New York Life Guaranteed | Trusted guaranteed coverage | $30,000 | 50–80+ | ~$25–$60 / ~$45–$110 | 2 years | Member discounts, strong backing |

| Physicians Mutual / Gerber | Simplified/guaranteed value | $5k–$30k | To 80–85 | $20–$50 / $35–$90 | 2 years (guaranteed) | Affordable final expense focus |

| State Farm Whole Life / GI | Agent service & permanent | Varies (GI ~$15k) | 45–80 / 50–75 | Competitive quoted / similar | Varies (GI 2 yrs) | Personalized advice, cash value |

Rates are illustrative based on April 2026 industry data and sample quotes. Actual premiums depend on health, gender, location, and exact product. Get personalized quotes for accuracy.

How to Choose the Right Life Insurance Policy for Seniors in 2026?

Use this expert checklist:

- Coverage needs: Aim for $10,000–$25,000+ to cover funerals plus extras.

- Health status: Guaranteed issue if health is poor; simplified or term if healthier.

- Budget and affordability: Fixed premiums that fit your retirement income—never increase in whole life/final expense.

- Waiting periods: Understand graded benefits in guaranteed policies.

- Cash value and features: Whole life builds savings you can access; some offer living benefits.

- Financial strength of carrier: Prioritize A or A+ AM Best ratings for claims reliability.

- Payout speed: Reputable carriers process claims quickly.

Compare at least 3–4 options and use your ZIP code and current health details for accurate quotes.

Common Mistakes Seniors Make When Buying Life Insurance in 2026

- Focusing only on the lowest advertised premium without verifying actual death benefit (e.g., unit pricing in some plans).

- Delaying purchase—rates and health issues worsen with time.

- Overlooking the graded benefit period in guaranteed issue policies.

- Not comparing multiple carriers or reading the full policy details.

- Assuming all “no medical exam” policies offer immediate full coverage.

- Buying without considering beneficiary needs or coordinating with existing coverage.

Conclusion

The 5 best life insurance policies for seniors in April 2026 provide practical, compassionate options tailored to varying health and budget needs. Whether you prioritize guaranteed issue life insurance for seniors, affordable burial insurance for seniors 2026, or competitive term coverage, acting now can lock in protection and bring reassurance to your family.

Finding the right life insurance policy as a senior in April 2026 doesn’t have to be complicated or stressful. The best choice depends on your health, budget, and family’s needs — and making the wrong decision can leave your loved ones unprotected. Our licensed senior life insurance specialists have helped thousands of families secure affordable, reliable coverage with minimal hassle. Get your free, no-obligation personalized quote and expert guidance today. Click here to speak with a senior life insurance specialist now.

Frequently Asked Questions (FAQ)

What are the 5 best life insurance policies for seniors in April 2026?

Mutual of Omaha, Pacific Life, AARP/New York Life, Physicians Mutual/Gerber, and State Farm frequently rank highly for accessibility, value, and senior-focused features.

Do I need a medical exam for senior life insurance?

Many guaranteed issue and simplified policies require no medical exam—only a few health questions or none at all.

What is the average cost of burial insurance for seniors in 2026?

For $10,000 coverage, expect roughly $20–$60/month at age 65 and $35–$110/month at age 75, varying by gender, health, and carrier.

Is guaranteed issue life insurance worth it?

Yes, if health conditions make other coverage difficult—it guarantees acceptance, though with a typical 2-year graded period.

How much burial insurance should I buy?

Enough to cover expected funeral costs ($8,300+ median) plus debts or extras—$10,000–$25,000 is common.

Can seniors over 80 get life insurance?

Yes—many final expense and guaranteed issue options extend to age 85, though premiums are higher and coverage more limited.

Does senior whole life insurance build cash value?

Yes, permanent whole life policies accumulate cash value over time on a tax-deferred basis.

How fast do final expense benefits pay out?

Most reputable carriers pay within days to a few weeks once required documentation is provided.