Many pre-retirees and new retirees feel overwhelmed when trying to decide between Medicare and private health insurance options. The transition from employer-sponsored coverage to retirement healthcare brings important questions about costs, benefits, networks, and predictability.

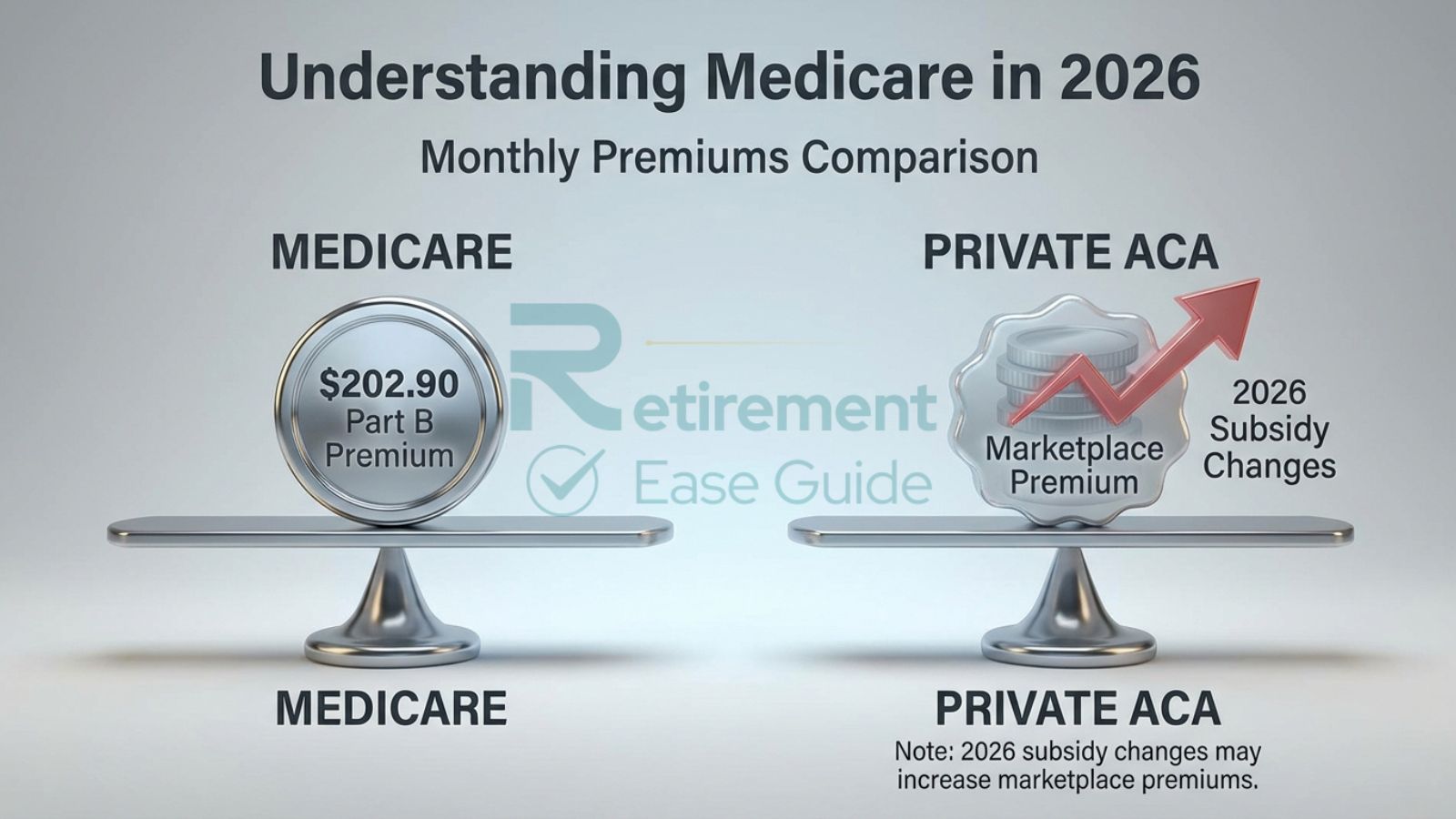

Medicare vs private insurance 2026 requires careful evaluation, especially with the standard Medicare Part B premium rising to $202.90 per month and the expiration of enhanced ACA premium tax credits causing significant premium increases for many Marketplace enrollees. This neutral guide breaks down the key differences to help you understand Medicare vs private health insurance 2026 and identify what may work best for your situation.

Understanding Medicare in 2026

Medicare is the federal health insurance program primarily serving people age 65 and older.

- Original Medicare consists of Part A (hospital insurance) and Part B (medical insurance). In 2026, the Part A deductible is $1,736 per benefit period, and Part B has a $283 annual deductible with 20% coinsurance on most services after the deductible. The standard Part B premium is $202.90 monthly, though higher-income beneficiaries pay more through Income-Related Monthly Adjustment Amounts (IRMAA), ranging up to $689.90.

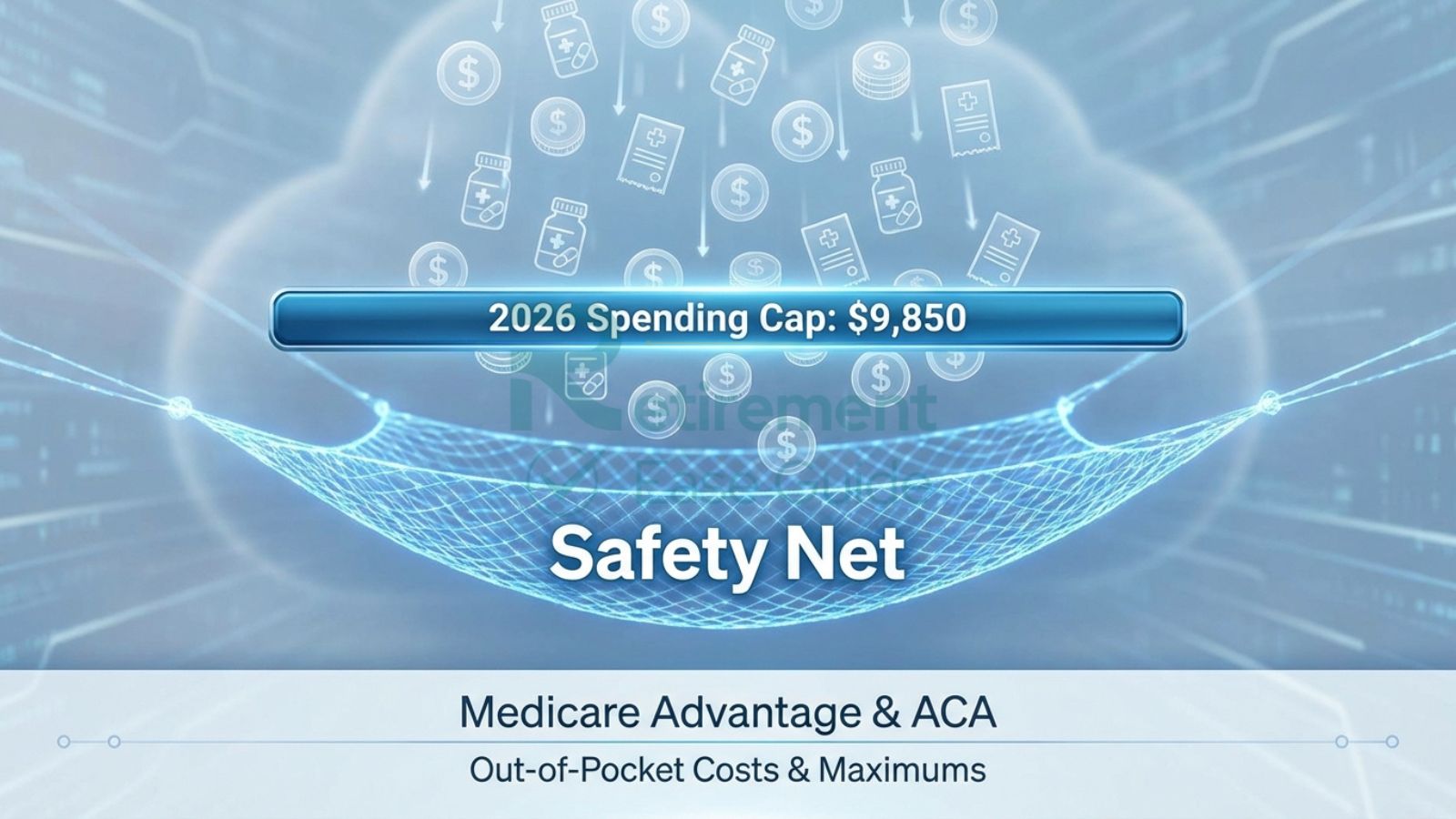

- Medicare Advantage (Part C): Private plans approved by Medicare that usually combine Parts A, B, and often D. Many feature $0 additional premium beyond Part B, with about two-thirds of MA-PD plans charging no extra monthly premium. Plans include an in-network out-of-pocket maximum (MOOP), with the 2026 maximum set at $9,850 in-network (median around $5,900 nationally, though actual plan limits vary).

- Part D Prescription Drug Coverage: Helps cover outpatient drugs, with a $2,100 annual out-of-pocket cap in 2026 (after which you pay $0 for covered Part D drugs for the rest of the year). The national base beneficiary premium is around $38.99, but actual plan premiums vary.

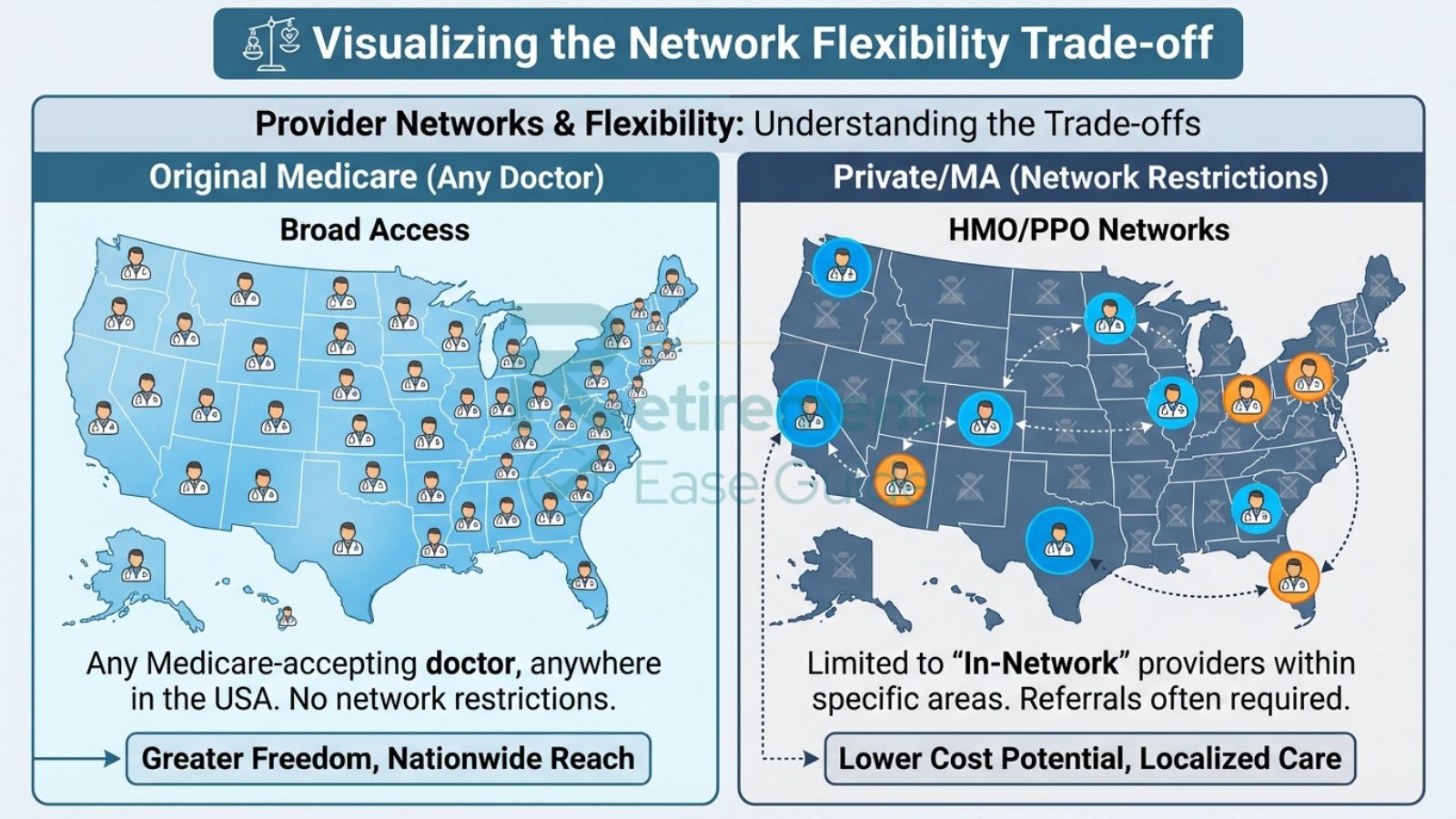

- Medigap (Medicare Supplement): Private policies that work with Original Medicare to cover gaps such as deductibles and coinsurance, offering more predictable costs but adding monthly premiums.

Medicare provides broad access to providers who accept it, with strong protections for prescription drugs once the out-of-pocket cap is reached.

Understanding Private Health Insurance in 2026

Private health insurance for individuals and families under 65 primarily comes through the ACA Marketplace, short-term plans, or remaining employer/retiree coverage.

- ACA Marketplace Plans: These offer essential health benefits with standardized metal tiers (Bronze through Platinum). With enhanced premium tax credits expiring after 2025, many enrollees face substantially higher net premiums in 2026—often more than doubling for those previously benefiting from expanded subsidies. Subsidies still exist up to 400% of the federal poverty level, but the previous “subsidy cliff” has returned for higher earners. Plans have annual out-of-pocket maximums (trending around $9,450 for individuals).

- Short-Term and Limited Plans: These typically have lower premiums but fewer protections, higher deductibles, and potential exclusions for pre-existing conditions. They serve as temporary bridges rather than comprehensive coverage.

- Other Individual or Retiree Policies: Some employers offer continued coverage, though these are less common.

Private plans emphasize flexibility and essential health benefits, with open enrollment periods and special enrollment for qualifying life events.

Medicare vs Private Insurance in 2026: Head-to-Head Comparison

Coverage & Benefits

Medicare offers standardized hospital and medical benefits with defined rules. Original Medicare has no overall annual spending cap unless supplemented, while Medicare Advantage provides bundled coverage with extras. Private ACA plans must cover essential health benefits (including hospitalization, preventive care, and maternity), but details vary by metal level and insurer.

Monthly Premiums

Medicare features a fixed Part B premium of $202.90 (plus possible IRMAA) with many Medicare Advantage plans adding $0–$14 on average. Private ACA premiums can vary widely; the loss of enhanced subsidies in 2026 often results in higher net costs for middle-income individuals, sometimes exceeding $500–$1,000+ monthly depending on age, location, and plan.

Out-of-Pocket Costs & Maximums

Original Medicare has no annual cap on 20% coinsurance (potentially leading to high costs without Medigap). Medicare Advantage caps in-network spending (up to $9,850 maximum in 2026). ACA plans have defined out-of-pocket maximums but often higher deductibles.

Provider Networks & Flexibility

Original Medicare + Medigap generally allows the broadest choice of any provider accepting Medicare. Medicare Advantage typically uses HMO or PPO networks. ACA plans vary—some offer broader networks, others narrower.

Prescription Drug Coverage

Medicare Part D or MA-PD includes a structured $2,100 out-of-pocket cap in 2026. ACA plans cover drugs as an essential benefit, but formularies, copays, and protections differ.

Extra Benefits (Dental, Vision, Hearing, Gym)

Medicare Advantage frequently bundles these (nearly universal in 2026), plus wellness programs. Original Medicare covers them minimally. ACA plans often provide limited adult dental/vision coverage or require separate policies.

Enrollment Periods

Medicare has an Initial Enrollment Period around age 65, Annual Enrollment (Oct 15–Dec 7), and Medicare Advantage Open Enrollment (Jan 1–Mar 31). ACA Marketplace has its own Open Enrollment window (typically Nov 1–Jan 15) with special periods for qualifying events.

Detailed Side-by-Side Comparison Tables

Table 1: Cost Comparison (Approximate 2026 National Figures – Actual Costs Vary by Location, Health, and Plan)

| Aspect | Medicare (Original + Typical Add-ons) | Private Insurance (ACA Marketplace) |

| Monthly Premium | Part B $202.90 + MA $0–$14 avg. + Part D ~$35–$40 | Often $100–$1,500+ (higher without subsidies post-2025 enhancements) |

| Deductible | Part A $1,736; Part B $283 | Frequently $1,000–$9,000+ by metal level |

| Out-of-Pocket Maximum | None for Original; MA up to $9,850 in-network | ~$9,450 individual (2026 trends) |

| Drug Out-of-Pocket Cap | $2,100 (Part D) | Varies by plan (no uniform federal cap like Part D) |

Table 2: Pros & Cons

| Option | Pros | Cons |

| Medicare | Standardized rules, broad provider access with Original + Medigap, drug cap, extras in MA | Part B premium increase, potential gaps without supplements, network limits in MA |

| Private Insurance | Essential health benefits, possible subsidies (though reduced), flexibility for under-65 | Higher premiums after subsidy changes, annual lock-in, variable deductibles |

Medicare Advantage vs ACA Marketplace Plans in 2026

This comparison is common for those nearing retirement. Medicare Advantage integrates care with extras like dental, vision, hearing, and a spending cap, often at low or $0 additional premium—but with network restrictions and possible prior authorization. ACA Marketplace plans cover essential benefits and may offer broader networks in some areas, but deductibles are typically higher and drug protections less structured than Part D. For those 65+, Medicare becomes the primary option; pre-65 individuals rely on ACA until eligibility. Many retirees find Medicare Advantage more predictable for ongoing care, while ACA suits younger or healthier pre-retirees when subsidies apply.

Who Should Choose Medicare in 2026?

Medicare often suits people turning 65 or older, particularly those with established provider relationships, moderate-to-high healthcare needs, or a desire for structured drug protections. It works well if you value extra benefits through Medicare Advantage or predictable gap coverage with Medigap. For more details on the top options, see our guide to the Best Medicare Advantage Plans in 2026.

Who Should Choose Private Insurance in 2026?

Private insurance, especially ACA Marketplace plans, is usually the main choice for those under 65. It may also appeal to individuals wanting specific network designs or coverage before Medicare eligibility, though the 2026 subsidy changes increase costs for many. Short-term plans can serve as temporary solutions but offer limited protections.

Key Factors to Consider + Related Retirement Planning Topics

When deciding, consider your age, income (affecting subsidies or IRMAA), health status, prescription needs, preferred doctors, travel plans, and budget for total costs—not just premiums.

Retirement healthcare planning extends beyond basic coverage. If you’re also thinking about protecting your family, don’t miss our article on the Best Senior Life Insurance Plans in 2026 and the 5 Best Life Insurance Policies for Seniors in 2026. Planning for future care needs? For those in Florida, local expertise can help—explore Medicare agents near me in Florida for personalized assistance.

Common Mistakes When Comparing Medicare vs Private Insurance

- Focusing only on premiums instead of total potential out-of-pocket costs.

- Assuming Medicare is “free” without accounting for Part B and possible supplements.

- Overlooking network restrictions or drug formularies.

- Missing enrollment deadlines and facing penalties.

- Not considering how 2026 subsidy changes affect ACA affordability.

- Relying on general advice without reviewing personal factors like medications and doctors.

Conclusion

Medicare vs private insurance 2026 has no single best answer—the right choice balances your age, health needs, budget, and lifestyle. With Part B premiums rising and ACA subsidy changes affecting affordability, thoughtful comparison helps secure suitable coverage for best health insurance for retirees 2026 and pre-retirees.

Deciding between Medicare and private insurance in 2026 is one of the most important healthcare decisions you will make for your retirement. The right choice depends on your age, health needs, budget, and lifestyle. Our licensed Medicare and health insurance specialists have helped thousands of individuals compare their options objectively and find the best coverage for their situation. Get your free, no-obligation personalized comparison and expert guidance today. Click here to speak with a Medicare and health insurance specialist now.

Frequently Asked Questions (FAQ)

Is Medicare better than private insurance in 2026?

It depends on your age and needs. Medicare often provides more predictable structure for those 65+, while private ACA plans serve pre-65 individuals.

How do costs compare in Medicare vs private health insurance 2026?

Medicare has a standard Part B premium of $202.90 with many low-cost MA options. ACA premiums have risen for many due to expired enhanced subsidies.

What about Medicare Advantage vs ACA plans 2026?

MA frequently includes extras and a spending cap; ACA emphasizes essential benefits with variable costs and networks.

Does Original Medicare vs private insurance offer more flexibility?

Original Medicare + Medigap generally provides the broadest provider choice.

Will private insurance cover pre-existing conditions?

ACA plans must; short-term plans may not.

When should I choose private insurance over Medicare?

Primarily before age 65 or when specific plan features align better with your situation.

How do enrollment periods differ?

Medicare and ACA each have distinct windows; missing them can limit options.