Deciding between Medicare Advantage vs Supplement Plans 2026 is one of the most common dilemmas retirees face. With the standard Medicare Part B premium at $202.90 per month and hundreds of plan options varying by county, many wonder whether a bundled Medicare Advantage (MA) plan or a Medicare Supplement (Medigap) policy paired with Original Medicare will better protect their health and wallet.

There is no universal “better” choice — it depends on your health needs, budget, preferred doctors, travel habits, and tolerance for out-of-pocket costs. This neutral guide explains both options clearly using 2026 data from CMS and Medicare.gov, so you can make a confident, informed decision.

Quick Overview of Medicare in 2026

Medicare is the federal health insurance program for most people age 65 and older. Original Medicare includes:

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care (with limits), hospice, and some home health. Most people pay $0 premium for Part A.

- Part B (Medical Insurance): Covers doctor visits, outpatient care, preventive services, and durable medical equipment. The standard monthly premium is $202.90 in 2026, with a $283 annual deductible and 20% coinsurance on most services after the deductible.

Original Medicare has no annual out-of-pocket maximum, so costs can add up without additional coverage. You can add a separate Part D prescription drug plan and/or a Medigap policy.

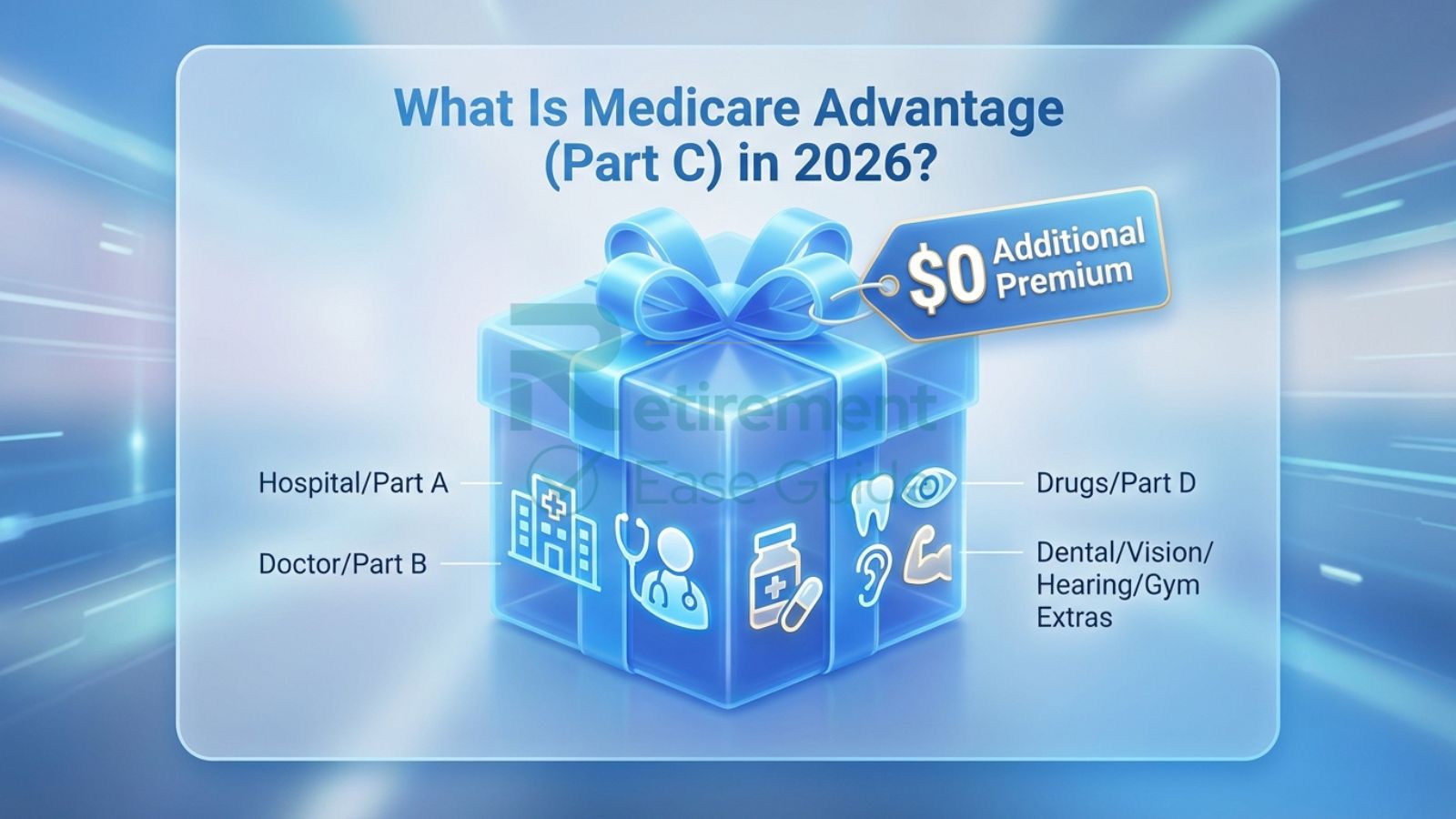

What Is Medicare Advantage (Part C) in 2026?

Medicare Advantage plans are private insurance plans approved by Medicare that provide all the benefits of Original Medicare (Parts A and B), and usually include Part D drug coverage. In 2026, the in-network out-of-pocket maximum (MOOP) is $9,250 (down from $9,350 in 2025), giving you a spending cap on covered services.

Many MA plans charge $0 additional premium beyond the Part B premium, with national averages for additional premiums remaining low (around $11–$14). Nearly all plans (98%+) offer some dental, vision, and hearing benefits, plus extras like fitness programs, transportation, or over-the-counter allowances. However, you typically must use in-network providers (except in emergencies), and plans may require prior authorization for certain services.

For a deeper look at standout options, see our guide to the Best Medicare Advantage Plans in 2026.

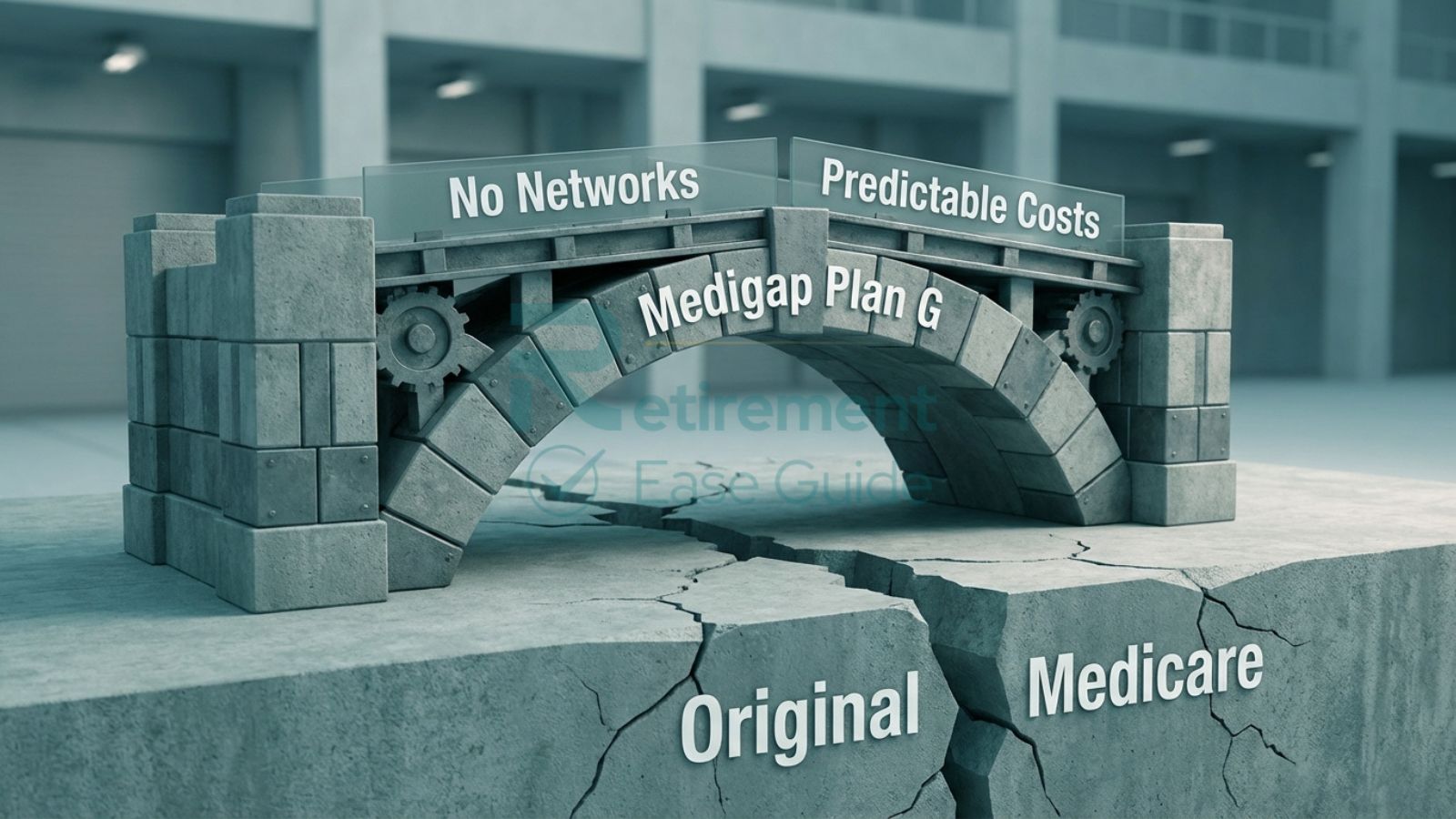

What Are Medicare Supplement (Medigap) Plans in 2026?

Medigap policies are standardized private insurance plans (labeled A through N, with some high-deductible versions) that work alongside Original Medicare to cover gaps such as the Part B deductible, coinsurance, and copayments. Benefits are identical for the same letter plan regardless of the insurance company — only premiums differ.

The most popular plans are Plan G (covers nearly all gaps except the Part B deductible) and Plan N (similar to G but with small copays for office visits and emergency room care). Average monthly premiums for Plan G at age 65 typically range from $150–$220, increasing with age and varying by location, gender, and insurer. Medigap offers excellent predictability because there is no network restriction — you can see any provider that accepts Medicare.

Medicare Advantage vs Medicare Supplement Plans in 2026: Head-to-Head Comparison

Monthly Premiums

- Medicare Advantage: Often $0 additional premium (you still pay the $202.90 Part B premium). Some plans may charge a small additional amount.

- Medigap: Adds $100–$300+ monthly on top of Part B (Plan G averages $150–$220 at age 65; Plan N is usually lower). You also need a separate Part D plan (average ~$35–$40 base premium).

Out-of-Pocket Costs

- Medicare Advantage: Capped at $9,250 in-network in 2026 (many plans set lower limits). You pay copays or coinsurance until you reach the cap.

- Medigap + Original Medicare: Very low or predictable out-of-pocket after the Part B deductible ($283). Plan G covers nearly everything after that; no annual cap needed because gaps are filled.

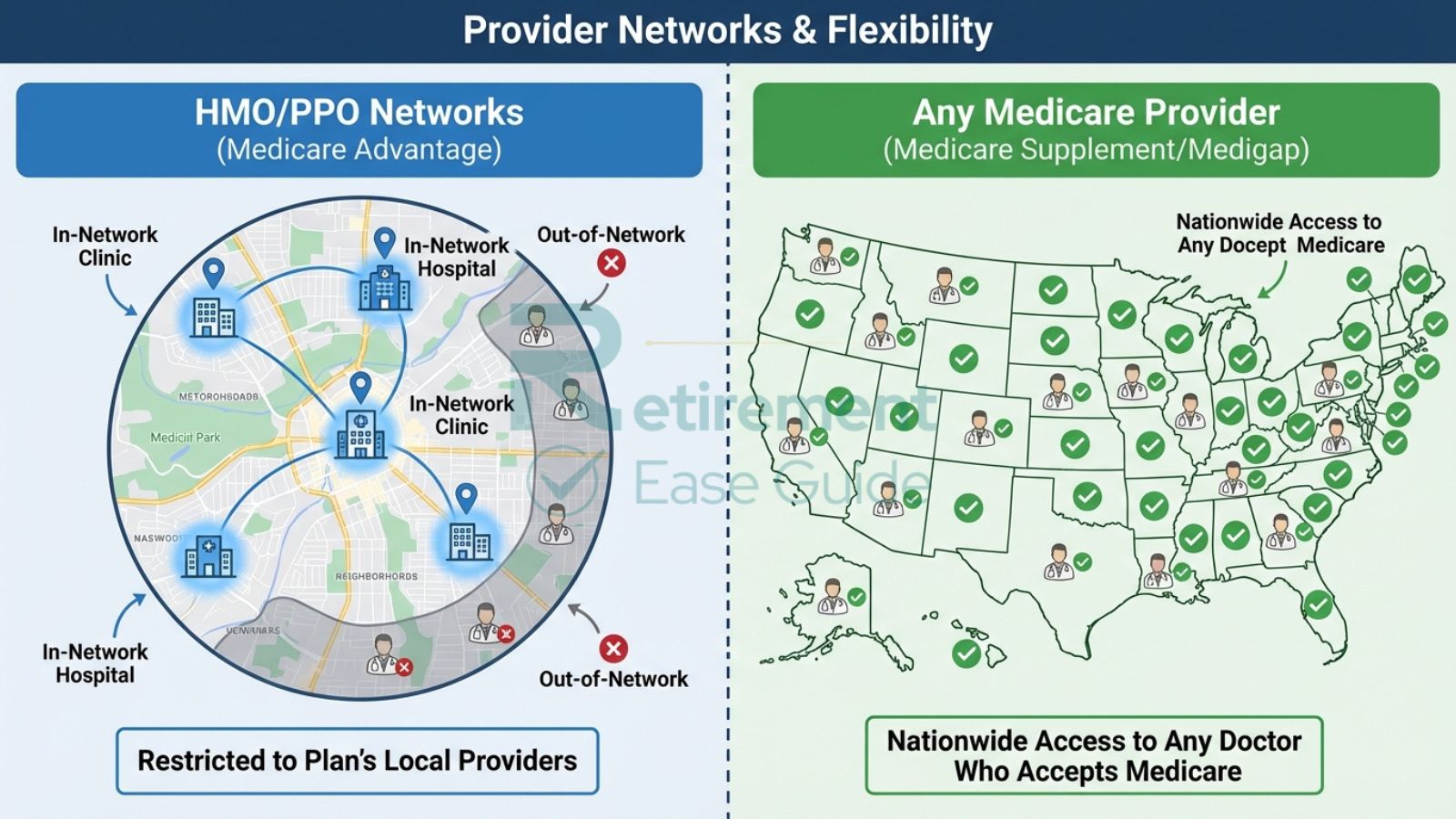

Provider Networks & Flexibility

- Medicare Advantage: Usually HMO or PPO networks. HMOs are more restrictive; PPOs offer more flexibility but at higher cost-sharing out-of-network.

- Medigap: Maximum flexibility — any doctor or hospital that accepts Medicare, anywhere in the U.S. Ideal for snowbirds or frequent travelers.

Extra Benefits (Dental, Vision, Hearing, Gym, etc.)

- Medicare Advantage: Strong advantage here. In 2026, 98%+ of plans offer dental, vision, and hearing benefits, often with allowances for cleanings, exams, eyewear, and hearing aids, plus gym memberships.

- Medigap: No extra benefits. Original Medicare covers routine dental, vision, and hearing very minimally.

Prescription Drug Coverage

- Medicare Advantage: Usually includes Part D. Plans have formularies and a $2,100 out-of-pocket cap in 2026.

- Medigap: Does not include drugs — you must buy a separate Part D plan.

Travel Coverage

- Medicare Advantage: Emergency coverage is required nationwide, but routine care is usually limited to the plan’s service area.

- Medigap: Full coverage anywhere Original Medicare is accepted, making it better for frequent travelers.

Predictability vs Flexibility

Medigap offers high predictability with low surprise bills. Medicare Advantage offers lower upfront premiums and extras but more variable costs depending on usage and network.

Detailed Side-by-Side Comparison Table (2026 Estimates)

Table 1: Cost Overview (National Averages/Typicals – Actual Costs Vary by Location, Age, Health, and Plan)

| Aspect | Medicare Advantage (Typical) | Medigap (Plan G + Part D) |

| Monthly Premium (beyond Part B) | $0 – $14 average | $150 – $220 (Plan G) + ~$35–$40 Part D |

| Part B Premium | $202.90 (standard) | $202.90 (standard) |

| Annual Deductible | Varies by plan (often $0 for many services) | $283 (Part B) |

| Out-of-Pocket Maximum | Up to $9,250 in-network | Very low/predictable after deductible |

| Typical Total Monthly Cost | $203 – $250 | $390 – $500+ |

Table 2: Pros & Cons Summary

| Option | Pros | Cons |

| Medicare Advantage | Lower premiums, extras (dental/vision/hearing), spending cap | Network restrictions, possible prior authorization, variable costs |

| Medigap + Original Medicare | Broad provider choice, predictable costs, no networks | Higher monthly premiums, no extras, separate Part D needed |

Pros and Cons of Medicare Advantage in 2026

Pros: Lower or $0 additional premiums, bundled drug coverage, popular extra benefits, annual out-of-pocket protection, and coordinated care in many plans.

Cons: Network limitations, potential changes in benefits or providers from year to year, and possible prior authorization requirements.

Pros and Cons of Medicare Supplement Plans in 2026

Pros: Excellent predictability, freedom to see almost any Medicare-accepting provider, no network issues, and strong protection against high medical bills.

Cons: Higher monthly premiums, no extra benefits like dental or vision, and the need for a separate Part D plan.

Who Should Choose Medicare Advantage vs Medigap in 2026?

Choose Medicare Advantage if:

- You want lower monthly premiums and value extras like dental, vision, and hearing.

- You are comfortable with network restrictions and staying mostly in your local area.

- You have predictable or moderate healthcare needs and want a spending cap.

- Budget is a primary concern upfront.

Choose Medigap (with Original Medicare) if:

- You travel frequently or want maximum provider flexibility.

- You prefer highly predictable costs with minimal surprise bills.

- You see specialists often or have providers outside typical MA networks.

- You are willing to pay higher premiums for peace of mind and freedom.

Many healthy retirees with local doctors lean toward MA for value and extras, while those with complex conditions or travel plans often prefer Medigap.

Other Important Retirement Protection Topics

Medicare decisions are only one piece of a solid retirement plan. Looking for budget-friendly overall options? Check out the Best Affordable Health Insurance for Retirees in 2026. Planning for future long-term care needs? Read our breakdown of How Much Does Long-Term Care Insurance Cost in 2026.

If you’re also thinking about protecting your family and legacy, don’t miss our article on the Best Senior Life Insurance Plans in 2026 and the 5 Best Life Insurance Policies for Seniors in 2026.

Common Mistakes Retirees Make When Choosing Between Medicare Advantage and Medigap

- Focusing only on premiums instead of total potential costs.

- Assuming all MA plans are the same or that Medigap includes extras.

- Switching without checking if current doctors remain in-network.

- Missing the Annual Enrollment Period (Oct 15–Dec 7) and getting locked into a suboptimal plan.

- Not considering future health changes or travel needs.

- Choosing based on advertising rather than personal needs and provider access.

Conclusion

Medicare Advantage vs Supplement Plans 2026 ultimately comes down to your personal circumstances. Medicare Advantage often provides great value through extras and lower premiums with a spending cap, while Medicare Supplement plans deliver unmatched flexibility and cost predictability.

Choosing between Medicare Advantage and Medicare Supplement plans in 2026 can feel overwhelming, but the right decision can save you thousands of dollars and provide better peace of mind. The best choice depends on your health, budget, travel plans, and preferred doctors. At Retirement Ease Guide Our licensed Medicare specialists have helped thousands of retirees compare these options and find the perfect fit. Get your free, no-obligation personalized Medicare Advantage vs Medigap review today. Click here to speak with a Medicare plan specialist now.

Frequently Asked Questions (FAQ)

What is the main difference between Medicare Advantage vs Medigap 2026?

Medicare Advantage bundles everything with possible extras and a spending cap but uses networks. Medigap fills gaps in Original Medicare for predictability and flexibility but costs more monthly and lacks extras.

Is Medicare Advantage vs Medicare Supplement vs Medigap cost comparison 2026 favorable to MA?

MA often wins on lower upfront premiums and extras, while Medigap wins on predictability and provider freedom. Total costs depend heavily on your healthcare usage.

Should I choose Medicare Advantage or Medigap in 2026?

It depends on your priorities. MA suits budget-conscious retirees who like bundled benefits; Medigap suits those who value flexibility and predictability.

Do Medigap plans cover dental and vision?

No — those are rarely covered. Medicare Advantage plans frequently do.

Can I switch between Medicare Advantage and Medigap?

Yes, during enrollment periods, but switching from MA to Medigap may require medical underwriting in some cases.

Are there best Medicare Supplement plans 2026 recommendations?

Plan G and Plan N are the most popular and comprehensive options available to new enrollees.

How do pros and cons of Medicare Advantage vs Supplement plans affect snowbirds?

Medigap generally works better for frequent travelers due to nationwide provider access.