Financial independence and retiring early — commonly known as FIRE — is an ambitious yet achievable goal for many Americans. It involves saving and investing aggressively enough to live off your portfolio without relying on traditional employment. In 2026, with updated contribution limits, evolving tax rules, and healthcare considerations, proper planning remains essential.

👉🔥 Start your FIRE journey with smart retirement planning tools and strategies.

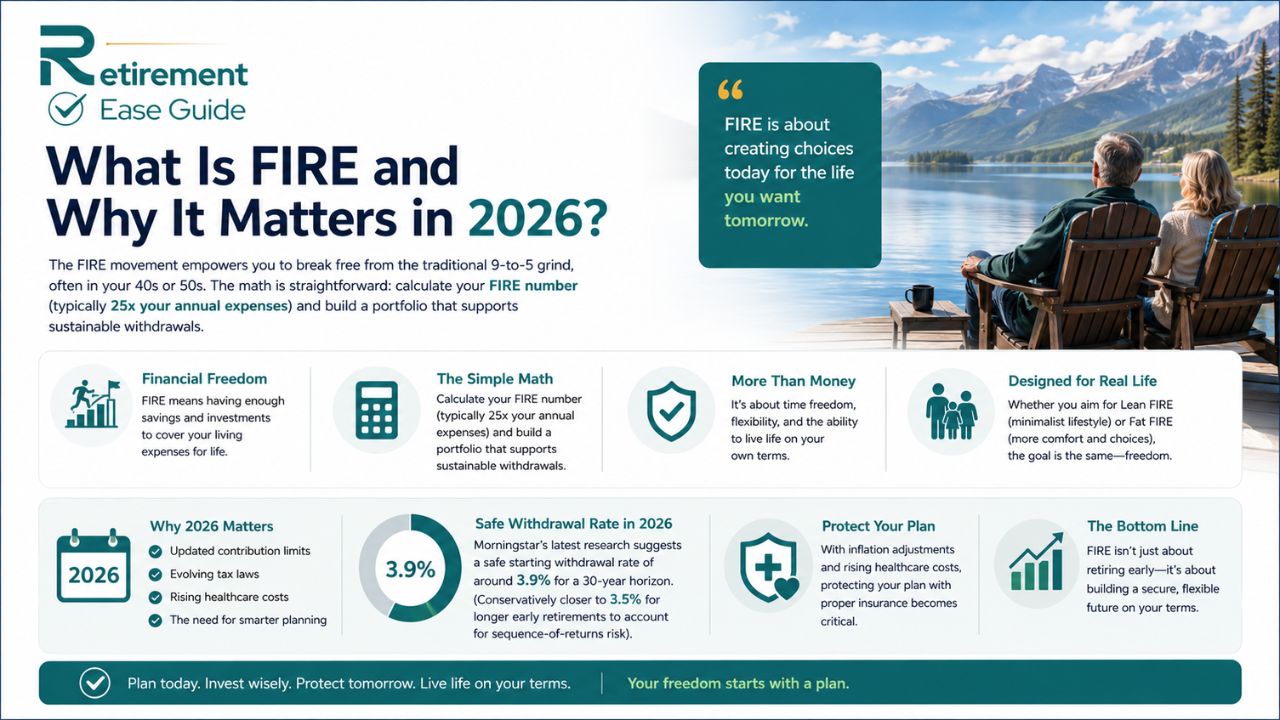

Whether you aim for Lean FIRE (minimalist lifestyle) or Fat FIRE (more comfortable spending), the core principles stay the same: high savings rate, smart investing, and risk protection. This guide outlines a practical, step-by-step approach tailored for 2026.

What Is FIRE and Why It Matters in 2026?

The FIRE movement empowers you to break free from the traditional 9-to-5 grind, often in your 40s or 50s. The math is straightforward: calculate your FIRE number (typically 25x your annual expenses) and build a portfolio that supports sustainable withdrawals.

In 2026, Morningstar’s latest research suggests a safe starting withdrawal rate of around 3.9% for a 30-year horizon (conservatively closer to 3.5% for longer early retirements to account for sequence-of-returns risk). With inflation adjustments and rising healthcare costs, protecting your plan with proper insurance becomes critical.

👉💰 Build wealth faster and achieve financial freedom with confidence.

Step 1: Calculate Your FIRE Number and Savings Rate

Start by tracking your current annual expenses. Multiply that by 25 to get your target portfolio size.

- Example: If you need $60,000 per year → FIRE number = $1.5 million.

Aim for a savings rate of 50% or higher of your income. This is much more aggressive than the traditional 10-15% recommendation but accelerates your timeline dramatically.

Maximize 2026 contribution limits:

- 401(k)/403(b): $24,500 (plus $8,000 catch-up if 50+, or $11,250 if 60-63)

- IRA: $7,500 (plus $1,100 catch-up if 50+)

👉🚀 Take the first step toward financial independence and early retirement.

Step 2: Adopt Tax-Efficient Investing Strategies

Invest in low-cost index funds, ETFs, and diversified portfolios. Focus on tax-advantaged accounts first, then taxable brokerage accounts. Consider Roth conversions and capital gains harvesting as part of your retirement tax planning.

Choose tax-friendly states if relocating. In 2026, top options include Florida, Tennessee, Texas, and South Dakota — states with no income tax that significantly boost your effective withdrawal power.

👉🏖️ Plan a stress-free early retirement with smarter money decisions today.

Step 3: Build Multiple Income Streams and Cut Expenses

Boost income through side hustles, career advancement, or real estate. Simultaneously reduce lifestyle inflation. Many successful FIRE practitioners practice geographic arbitrage — living in lower-cost areas while earning high incomes remotely.

Step 4: Protect Your Plan with Insurance and Risk Management

Early retirement means a longer period without employer benefits, making protection vital.

One key area is life insurance. Explore the 5 best life insurance policies for seniors to safeguard your family and legacy.

Long-term care is another major risk. Understanding how much long-term care insurance costs helps you budget realistically and avoid depleting your nest egg.

Step 5: Navigate Healthcare in Early Retirement

Healthcare often represents the biggest wildcard before Medicare eligibility at age 65.

Compare options carefully. Many early retirees use a combination of strategies until Medicare kicks in. Discover the best affordable health insurance for retirees to bridge this gap effectively.

Once eligible for Medicare, choosing the right path is crucial. Learn the differences in Medicare vs. private insurance and decide what fits your situation.

A common dilemma is choosing between plans. Compare Medicare Advantage vs. Medicare Supplement plans to understand coverage, costs, and flexibility.

If you retire in a popular state like Florida, local expertise helps. Find Medicare agents near me in Florida for personalized enrollment support.

Step 6: Choose the Right Insurance Products

For life insurance needs in retirement, understand the trade-offs. Compare term vs. whole life insurance for seniors to select the policy that aligns with your goals and budget.

Work with reputable carriers. Review the best insurance companies for seniors to ensure reliability and strong claims service.

👉💼 Learn how to save aggressively and retire years earlier than expected.

Step 7: Monitor, Adjust, and Enjoy Financial Freedom

Review your plan annually. Use guardrails — reduce spending in down markets and enjoy modest increases in strong ones. Build a 6–12 month emergency fund in liquid accounts.

Conclusion

Achieving financial independence and retiring early requires discipline, smart planning, and proactive risk management. By following these steps and protecting your wealth with the right strategies, you can create the freedom you desire.

At Retirement Ease Guide, we’re here to support your journey with free tools, expert guides, and connections to trusted professionals. Take the next step today — explore our retirement calculators, compare options, or reach out to an advisor to customize your FIRE plan.

FAQs About Financial Independence and Early Retirement

- How much do I need to retire early in 2026?

Most people target 25x their annual expenses. For a $50,000 lifestyle, you’ll need about $1.25 million. Adjust higher for longer retirements or healthcare buffers.

- Is the 4% rule still safe?

For traditional retirements, around 3.9% is considered safe in 2026. Early retirees often plan more conservatively at 3.5% due to longer time horizons.

- What role does health insurance play in FIRE?

It’s one of the biggest expenses. Proper planning with affordable options and Medicare strategies can save tens of thousands.

- Should I move to a different state for FIRE?

Yes, if it lowers taxes and living costs. Florida and Tennessee are popular for their tax advantages.

- Do I still need life insurance after achieving FIRE?

It depends on your obligations. Many use it for legacy planning or spousal protection.

- How long does it typically take to reach FIRE?

With a 50%+ savings rate, many achieve it in 10–17 years, depending on starting income and expenses.

- What are the biggest risks in early retirement?

Sequence of returns risk, healthcare costs, and inflation. Diversification and insurance mitigate these.