As you or a loved one approaches or navigates the senior years, the question of life insurance often resurfaces with new urgency. Many seniors and their adult children wonder whether to choose temporary, affordable protection or lifelong coverage that offers additional features. The dilemma of term vs whole life insurance for seniors is common, especially in 2026 when healthcare costs, funeral expenses, and legacy goals remain top concerns for families on fixed incomes.

Term vs whole life insurance for seniors boils down to your specific needs: short-term financial protection versus permanent coverage with potential cash value. Term life provides high coverage at lower cost for a set period, while whole life delivers lifelong protection and builds savings you or your beneficiaries can access. Understanding the differences helps bring peace of mind that your family won’t face unnecessary financial burdens. This guide offers a clear, empathetic comparison based on 2026 products, rates, and trends to support informed decisions.

Understanding Term Life Insurance for Seniors

Term life insurance delivers coverage for a specific period—typically 10, 15, 20, or 30 years, though options shorten for older applicants. If you pass away during the term, your beneficiaries receive the death benefit. The policy expires at the end of the term unless renewed or converted (where available).

For seniors, term life works best for covering temporary needs such as remaining mortgage balances, debts, or income replacement for a surviving spouse during a transition period. Premiums stay level during the term and are significantly lower than permanent options, making coverage more accessible. However, renewability becomes limited or expensive after age 70–80, and many carriers cap issue ages around 70–80 for new term policies.

Underwriting usually involves a medical exam or health questions for better rates, though some no-exam options exist. In 2026, term remains popular for healthier seniors seeking maximum coverage per dollar spent.

Understanding Whole Life Insurance for Seniors

Whole life insurance provides permanent coverage for your entire lifetime as long as premiums are paid. Premiums remain fixed, and the policy builds cash value over time on a tax-deferred basis. You can borrow against or withdraw from this cash value while alive, and the death benefit passes to beneficiaries income-tax-free in most cases.

For seniors, whole life (including variations like final expense or burial insurance) offers guaranteed lifelong protection without the worry of policy expiration. It suits goals such as covering final expenses, leaving a legacy, or providing supplemental funds. Many seniors choose smaller whole life policies focused on end-of-life costs, as larger traditional whole life becomes quite expensive with age.

Cash value life insurance for seniors grows predictably but at a modest rate. Underwriting ranges from fully medical to simplified or guaranteed issue. In 2026, whole life appeals to those wanting certainty and potential living benefits.

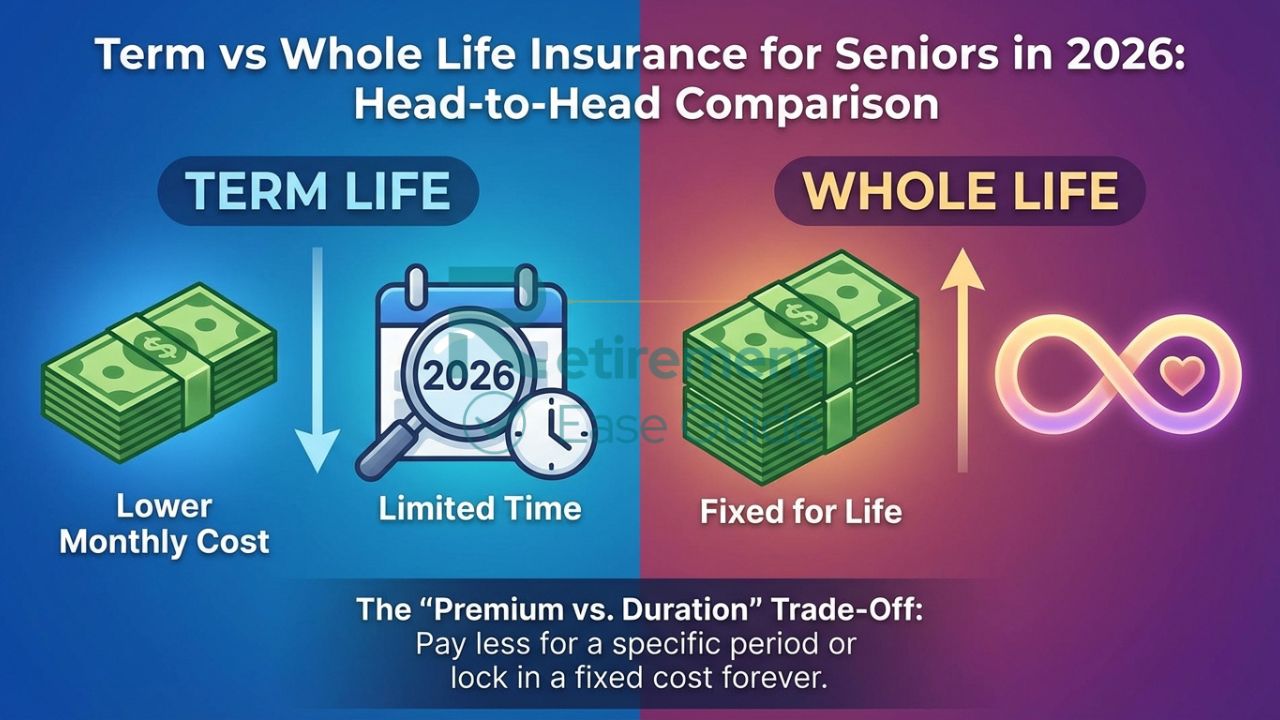

Term vs Whole Life Insurance for Seniors in 2026: Head-to-Head Comparison

Several key factors distinguish the two options for seniors ages 50–85:

- Coverage Duration: Term lasts a set number of years and then ends. Whole life lasts your lifetime.

- Premiums: Term offers much lower monthly costs, especially for shorter terms or healthier applicants. Whole life premiums are higher but fixed and guaranteed never to increase.

- Cash Value: Term has none. Whole life builds cash value that grows over time and can be accessed via loans or withdrawals.

- Death Benefit: Both pay a tax-free benefit to beneficiaries, but term only if death occurs during the active term. Whole life guarantees payout (subject to policy terms).

- Underwriting: Term often requires medical exams for best rates. Whole life for seniors frequently uses simplified issue or guaranteed issue, making it easier to obtain with health challenges.

- Renewability/Convertibility: Many term policies allow conversion to whole life within a certain window, but renewal rates skyrocket with age. Whole life needs no renewal.

- Suitability for Seniors: Term suits temporary gaps or budget-conscious needs. Whole life (or its final expense variants) better addresses permanent concerns like burial costs and legacy.

Final expense insurance vs whole life is a common discussion—final expense policies are simplified or guaranteed whole life designed specifically for smaller end-of-life needs.

Detailed Side-by-Side Comparison Tables

Table 1: Term vs Whole Life Insurance for Seniors – Key Features

| Feature | Term Life Insurance for Seniors | Whole Life Insurance for Seniors |

| Coverage Duration | 10–30 years (limited availability after 70) | Lifetime (as long as premiums paid) |

| Premiums | Lower, level during term | Higher, fixed for life |

| Cash Value | None | Builds over time, accessible while alive |

| Death Benefit Guarantee | Only if death during term | Guaranteed for life |

| Underwriting | Often medical exam or health questions | Simplified or guaranteed issue common |

| Best For Seniors | Temporary debts, mortgage, short-term needs | Final expenses, legacy, lifelong protection |

| Renewability | Limited and expensive at older ages | Not needed |

Table 2: Sample Monthly Premiums in 2026 (Illustrative Averages – Non-Tobacco, Healthy/Preferred Where Applicable)

These are approximate 2026 figures based on industry data. Actual rates depend on health, gender, location, and exact carrier. Term examples assume 10–20 year terms where available; whole life/final expense uses smaller face amounts common for seniors.

| Age / Coverage Example | Term Life (e.g., $100k–$250k, 10–20 yr) | Whole Life / Final Expense (e.g., $10k–$25k) |

| Age 65 Female | $30–$80/month | $22–$50/month |

| Age 65 Male | $40–$120/month | $29–$65/month |

| Age 75 Female | $100–$300+/month (limited terms) | $37–$90/month |

| Age 75 Male | $150–$450+/month (limited terms) | $50–$120/month |

For larger whole life amounts, premiums rise substantially. Guaranteed issue policies cost more per benefit dollar due to no health questions.

Pros and Cons of Term Life Insurance for Seniors

Pros:

- Significantly more affordable, allowing higher coverage amounts.

- Simple and straightforward for temporary needs.

- Convertible to permanent coverage in many cases during early years.

- Ideal if you have specific debts or obligations that will end.

Cons:

- Expires without payout if you outlive the term.

- Renewal or new coverage at older ages becomes very expensive or unavailable.

- No cash value or living benefits.

- Limited options for seniors over 70–75.

Pros and Cons of Whole Life Insurance for Seniors

Pros:

- Lifelong coverage with no expiration worry.

- Fixed premiums that never increase.

- Builds cash value for potential loans, withdrawals, or supplemental retirement income.

- Guaranteed death benefit for final expenses or legacy.

- Easier approval via simplified or guaranteed issue options.

Cons:

- Higher premiums reduce affordability for large coverage amounts.

- Cash value growth is modest compared to other investments.

- Overpaying for coverage if needs are purely temporary.

- Smaller face amounts in guaranteed issue policies.

When Should Seniors Choose Term Life Insurance?

Term life makes sense for seniors who:

- Have a remaining mortgage or other time-limited debts.

- Want to supplement income replacement for a spouse during a transition period.

- Are in good health and can qualify for competitive rates.

- Prefer lower premiums to free up budget for other retirement needs.

It works well in your 50s or early 60s but becomes less practical as options shrink after age 70. Always check convertibility features if you anticipate future permanent needs.

When Should Seniors Choose Whole Life Insurance?

Whole life (including final expense insurance) is often preferable when you want:

- Guaranteed lifelong protection without renewal concerns.

- Coverage for final expenses, medical bills, or burial costs (median funeral ~$8,300–$13,000+ with extras).

- A small legacy or inheritance for children/grandchildren.

- Cash value as a potential emergency fund or supplement.

Affordable life insurance for seniors over 65 frequently points to whole life variants. Guaranteed issue life insurance ensures acceptance regardless of health, though with graded benefits (limited payout in first 2 years) and higher relative cost.

Hybrid Approaches and Alternatives for Seniors

Many seniors combine or choose hybrid solutions:

- Simplified Issue: Answers a few health questions, no full exam—faster approval with moderate coverage.

- Guaranteed Issue: No questions or exam; ideal for serious health issues but with smaller limits and possible waiting periods.

- Conversion from term to whole life during the convertible period.

- Final expense policies as streamlined whole life focused on burial costs.

These options balance accessibility and cost for seniors who may not qualify for traditional underwriting.

Related Retirement Insurance Planning Topics

Life insurance decisions fit into broader retirement strategies. For comprehensive options tailored to seniors, explore our guide to the Best Senior Life Insurance Plans in 2026. If you want specific carrier recommendations and expert picks, review the 5 Best Life Insurance Policies for Seniors in 2026.

Common Mistakes Seniors Make When Choosing Between Term and Whole Life

- Focusing solely on the lowest premium without considering total value or expiration risk.

- Assuming term will always be renewable affordably at older ages.

- Overlooking the graded benefit period in guaranteed issue policies.

- Buying more coverage than needed, straining fixed retirement income.

- Not reviewing beneficiary needs or coordinating with existing policies.

- Delaying purchase—rates and health issues worsen with time.

Conclusion

Term vs whole life insurance for seniors ultimately depends on whether your priority is affordable temporary protection or guaranteed lifelong coverage with added features. Both play valuable roles in retirement planning, and many families benefit from a thoughtful mix or hybrid approach.

Choosing between term vs whole life insurance for seniors in 2026 is a deeply personal decision that depends on your health, budget, and what you want to leave behind for your loved ones. Making the right choice can provide valuable peace of mind. At Retirement Ease Guide our licensed senior life insurance specialists have helped thousands of seniors and their families find the most suitable and affordable coverage. Get your free, no-obligation personalized life insurance review today. Click here to speak with a senior life insurance specialist now.

Frequently Asked Questions (FAQ)

What is the main difference in term vs whole life insurance for seniors?

Term provides temporary coverage at lower cost; whole life offers permanent protection and builds cash value.

Is term life insurance for seniors 2026 still available?

Yes, but options decrease after age 70, with shorter terms and higher rates.

How much more expensive is whole life insurance for seniors 2026?

Whole life (especially final expense) typically costs 5–15 times more per $1,000 of coverage than term, but provides lifelong guarantees.

Can seniors over 65 get affordable life insurance?

Yes—simplified and guaranteed issue whole life or final expense policies keep options accessible.

Does whole life insurance build cash value for seniors?

Yes, though growth is gradual; it can be accessed for living needs.

Is guaranteed issue life insurance a good alternative?

It ensures acceptance for those with health challenges, though with smaller coverage and possible waiting periods.

Should I choose term or whole life if I have final expenses in mind?

Whole life or final expense policies are usually better for permanent end-of-life needs.

Can I convert term life to whole life later?

Many policies allow conversion within a specified period without new underwriting.