Turning 65 or already navigating retirement brings many rewards, but healthcare costs often rank among the biggest worries. Medical expenses can quickly add up, especially with frequent doctor visits, prescription drugs, or unexpected hospital stays. In 2026, understanding your best health insurance options for seniors age 65+ in the US empowers you to protect your health and savings without unnecessary stress.

Most Americans 65 and older rely on Medicare, the federal health insurance program. The main paths include Original Medicare (Parts A and B) paired with a Medigap supplement and standalone Part D drug plan, or an all-in-one Medicare Advantage (Part C) plan. Some explore employer retiree coverage or other alternatives, but the vast majority choose between these two primary routes.

Key 2026 updates include:

- Part B standard monthly premium: $202.90 (up from $185 in 2025).

- Part B annual deductible: $283.

- Part A inpatient hospital deductible: $1,736.

- Medicare Advantage average monthly premium (in addition to Part B): around $14, with many plans at $0 premium.

- Medicare Advantage out-of-pocket maximum for in-network services: $9,250 (slightly lower than 2025).

- Part D continues evolving with a $2,100 annual out-of-pocket cap on covered drugs (after any deductible), helping limit catastrophic costs.

These figures provide a clearer picture as you compare Medicare options 2026. Remember, this article is for educational purposes only and not personalized advice. Consult a licensed Medicare specialist or advisor for your situation.

Understanding Original Medicare (Parts A & B)

Original Medicare forms the foundation for many seniors. Part A covers inpatient hospital care, skilled nursing facility stays (with limits), hospice, and some home health services. Part B covers outpatient care, doctor visits, preventive services, durable medical equipment, and more.

In 2026, after meeting deductibles, you typically pay 20% coinsurance on most Part B services with no annual out-of-pocket limit unless you add supplemental coverage. This “20% forever” aspect concerns many retirees, as serious illness could lead to high costs.

Limitations include no routine dental, vision, or hearing coverage, and limited prescription drug benefits (none in Original Medicare itself). You can see any provider that accepts Medicare nationwide, offering excellent flexibility. Many add a Medigap policy to cover gaps and a separate Part D plan for drugs.

Option 1: Original Medicare + Medigap (Medicare Supplement) + Part D

This combination gives broad protection. You keep Original Medicare and buy a Medigap policy from a private insurer to pay many out-of-pocket costs. You then add a standalone Part D prescription drug plan.

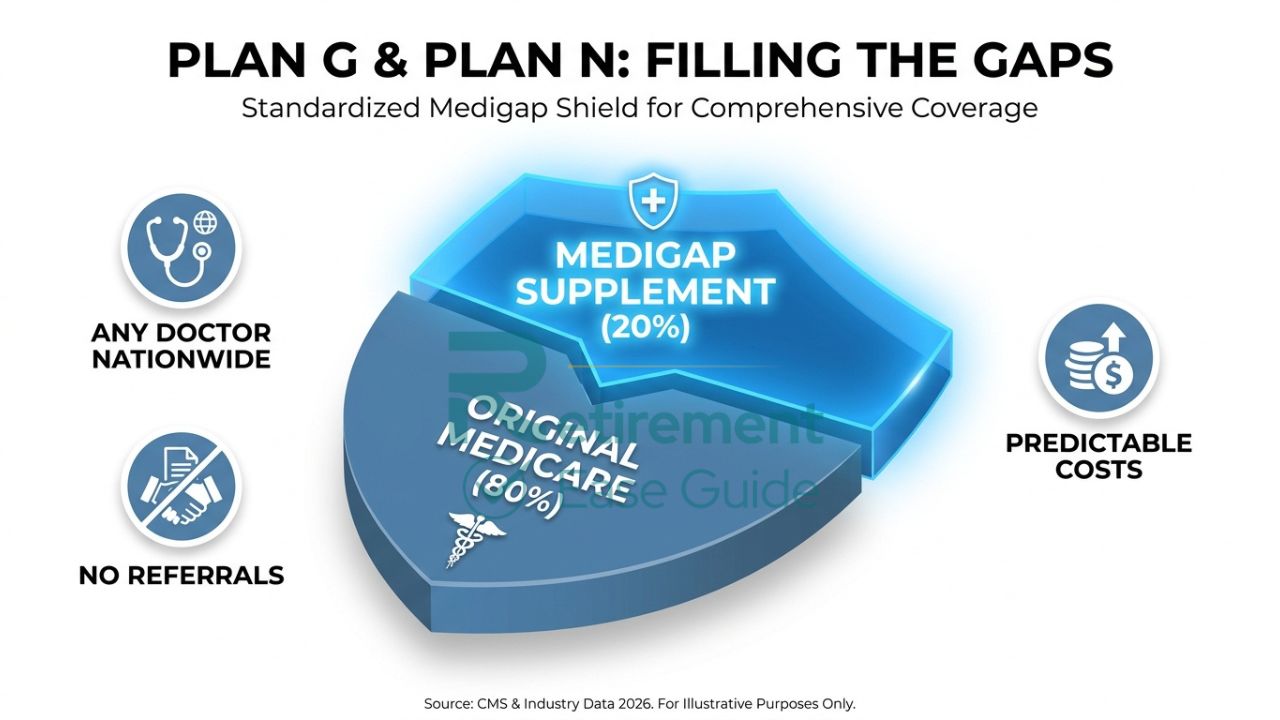

How Medigap works: Standardized plans (labeled A through N) are sold by private companies but must follow federal rules. They help pay deductibles, coinsurance, and copayments that Original Medicare leaves behind. You pay a monthly Medigap premium, which varies by plan, age, gender, location, and tobacco use.

The most popular plans in 2026 remain Plan G and Plan N for new enrollees (those eligible for Medicare on or after January 1, 2020 cannot buy Plan F).

- Plan G: Covers the Part A deductible, Part B coinsurance (after the $283 deductible), foreign travel emergencies, and more. It offers near-complete gap coverage but does not cover the Part B deductible. Many consider it the gold standard for comprehensive protection.

- Plan N: Similar to G but with small copays for doctor visits ($20) and emergency room visits ($50, waived if admitted). It usually costs less in premiums and remains popular for budget-conscious seniors who don’t mind minor copays.

Pros:

- Predictable costs with little or no coinsurance after premiums and deductibles.

- Freedom to see any Medicare-accepting doctor or hospital nationwide.

- No network restrictions or referrals needed for specialists.

Cons:

- Higher total premiums (Part B + Medigap + Part D).

- No routine coverage for dental, vision, or hearing (though some Medigap plans offer limited foreign travel emergency benefits).

- You handle claims yourself in some cases, though most are straightforward.

This option suits best those who value maximum provider choice, travel frequently within the U.S., or want protection against high medical bills without worrying about networks or prior authorizations. It works especially well for healthier individuals or those with established doctors they wish to keep long-term.

If considering broader retirement protection, many explore senior life insurance plans 2026 alongside health coverage to help safeguard loved ones financially.

Option 2: Medicare Advantage Plans (Part C)

Medicare Advantage plans, offered by private insurers approved by Medicare, serve as an alternative to Original Medicare. They must cover at least what Original Medicare provides (Parts A and B), and most include Part D drug coverage. Many bundle extra benefits.

In 2026, trends show continued affordability with lower average premiums and robust supplemental offerings. Most plans provide dental, vision, and hearing benefits—areas Original Medicare largely ignores. Additional perks often include fitness programs (like SilverSneakers), over-the-counter allowances, meal delivery, or transportation to appointments, though availability and generosity vary by plan and may shift slightly year to year.

HMO vs. PPO:

- HMO plans generally require using in-network providers (except emergencies) and often need referrals for specialists. They tend to have lower premiums and out-of-pocket costs.

- PPO plans offer more flexibility with out-of-network coverage (at higher cost) and usually no referrals.

Pros:

- Often $0 or low additional premium beyond Part B.

- Annual out-of-pocket maximum ($9,250 or less for in-network in 2026) caps your spending.

- Extra benefits for dental, vision, hearing, and wellness.

- Simplified claims in many cases.

Cons:

- Network restrictions can limit doctor or hospital choices.

- Prior authorizations may be required for some services.

- Plans can change benefits, premiums, or networks annually.

- Less flexibility if you travel or move.

Medicare Advantage appeals to those who want lower upfront costs, value extra benefits, and primarily use in-network providers. Many strong carriers compete in this space; resources on top medicare providers in usa 2026 can help identify highly rated options in your area.

Direct Comparison: Medicare Advantage vs. Original Medicare + Medigap in 2026

Choosing between these paths depends on your health needs, budget, preferred doctors, and lifestyle. Here’s a side-by-side view:

| Aspect | Original Medicare + Medigap + Part D | Medicare Advantage (Part C) |

| Monthly Premiums | Part B ($202.90) + Medigap ($100–$300+) + Part D (~$30–$60 avg.) | Part B ($202.90) + plan premium (avg. ~$14, many $0) |

| Out-of-Pocket Costs | Low after Medigap (mainly deductibles + premiums); no annual cap without Medigap | Varies; capped at $9,250 (or less) for in-network services |

| Doctor Choice | Any Medicare-accepting provider nationwide | Usually network-based (HMO stricter; PPO more flexible) |

| Drug Coverage | Separate Part D plan | Usually included; integrated with medical benefits |

| Extra Benefits | Limited (some foreign travel); add-ons rare | Often includes dental, vision, hearing, fitness, OTC, etc. |

| Flexibility | High; easy to travel or switch providers | Lower in-network focus; may need approvals |

For deeper insights into trade-offs, many seniors review detailed comparisons of medicare advantage vs supplement plans 2026.

Real-life scenarios:

- Scenario 1: Sarah, 68, lives in a rural area with her longtime cardiologist who accepts Medicare. She travels often and wants zero surprises on bills. Original Medicare + Plan G + Part D gives her peace of mind and flexibility.

- Scenario 2: Robert, 67, stays local, takes several prescriptions, and wants dental coverage without high premiums. A $0-premium Medicare Advantage PPO with strong drug and dental benefits fits his needs and budget better.

If affordability remains a priority while exploring options, some compare against best affordable health insurance for retirees 2026.

Other Important Factors to Consider in 2026

Prescription drug coverage: Part D remains essential. In 2026, the out-of-pocket cap sits at $2,100 for covered drugs, with a maximum deductible of $615 (many plans have $0). Medicare continues negotiating prices on select high-cost drugs, potentially lowering costs further. Compare formularies carefully—your medications must be covered at reasonable tiers.

Dental, vision, and hearing benefits: Original Medicare offers little here, making Medigap + Part D less comprehensive without add-ons. Medicare Advantage frequently includes these, though coverage levels (e.g., annual dollar maximums for dental) vary widely. Review specifics, as “included” does not always mean fully covered.

Provider networks and plan quality: Check if your doctors are in-network for Advantage plans. Star ratings from Medicare (1–5 stars) indicate quality, complaints, and member experience. Consider plan stability—some carriers adjust networks or benefits yearly.

For those worried about extended care needs beyond standard health insurance, exploring How Much Does Long-Term Care Insurance Cost in 2026? provides valuable context for comprehensive planning.

How to Choose the Best Health Insurance Option for You?

Follow this step-by-step checklist:

- Assess your current situation: List your doctors, hospitals, medications, and expected needs (e.g., frequent specialist visits or dental work).

- Estimate costs: Factor premiums, deductibles, copays, and potential out-of-pocket maximums. Use Medicare’s Plan Finder tool at Medicare.gov.

- Compare benefits: Prioritize what matters most—provider choice, drug coverage, extra perks, or lowest predictable costs.

- Check eligibility and timing: Initial enrollment at 65 is key; special periods apply for changes. Avoid late penalties.

- Review carrier reliability: Look into best insurance companies for seniors 2026 for financial strength and customer service.

- Consider life insurance integration: As part of broader planning, evaluate how health coverage fits with term vs whole life insurance for seniors to protect assets and heirs.

Ask yourself:

- Do I prefer flexibility or lower premiums with extras?

- Are my current providers in a plan’s network?

- How much can I comfortably spend monthly versus in a crisis?

Common Mistakes to Avoid When Choosing Medicare Coverage in 2026

- Assuming all plans are the same—details matter greatly by location and personal needs.

- Ignoring network restrictions or prior authorization rules in Advantage plans.

- Forgetting to re-evaluate annually during Open Enrollment (Oct 15–Dec 7).

- Overlooking Part D formulary changes that could raise drug costs.

- Delaying enrollment and facing penalties.

- Choosing based only on premium without considering total costs or benefits.

Taking time now prevents regret later.

At Retirement Ease Guide we connect you with licensed insurance specialists who have helped thousands of retirees find affordable Medicare Advantage plans with the right coverage options for their needs and budget. Get your free, no-obligation personalized Medicare Advantage plan comparison today. Click here to speak with a Medicare plan specialist now.