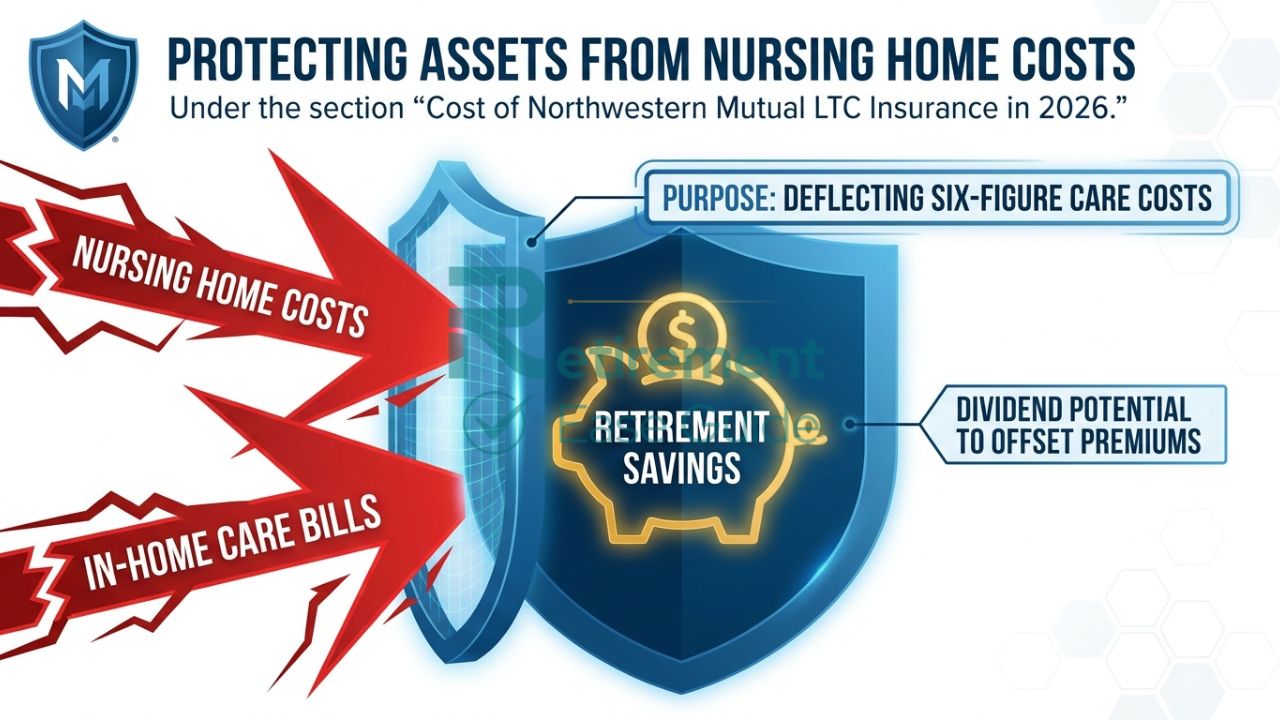

Long-term care insurance helps pay for services many people need as they age—assisted living, in-home care, nursing home stays, or adult day programs—that Medicare and most health insurance do not fully cover. For seniors and pre-retirees ages 55–79, planning ahead is critical because the average lifetime cost of formal long-term care can easily reach six figures, potentially draining retirement savings and placing burdens on family members.

Northwestern Mutual LTC insurance stands out in 2026 as a premium option backed by one of the strongest financial companies in the industry. It offers both a traditional standalone policy (QuietCare) and hybrid life insurance policies with long-term care riders. With exceptional financial strength ratings—including A++ from A.M. Best and top marks from Moody’s, S&P Global, and Fitch—Northwestern Mutual frequently appears on “best LTC insurance” lists, especially for couples seeking generous discounts and high benefit limits. This review presents a balanced look at its offerings, costs, pros and cons, and whether it makes sense for your situation in 2026.

Types of Long-Term Care Insurance Offered by Northwestern Mutual in 2026

Northwestern Mutual provides two main approaches to long-term care protection.

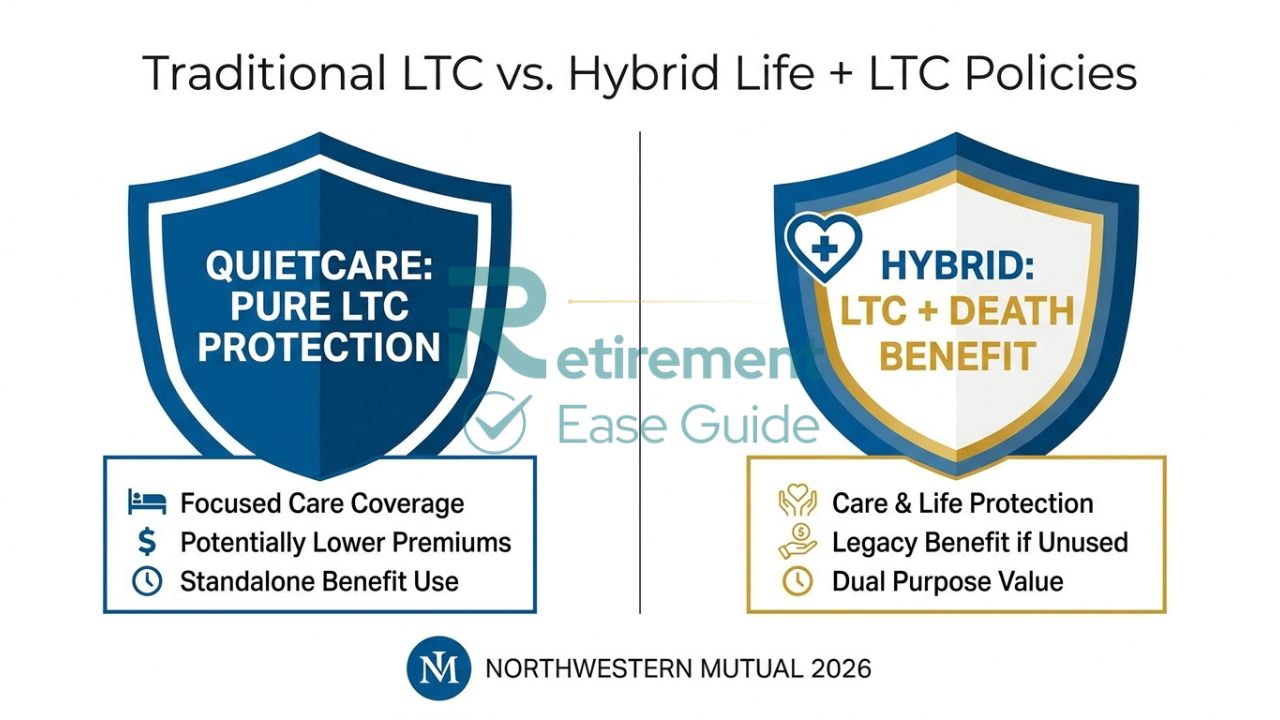

Standalone LTC: QuietCare Policy

QuietCare is a traditional long-term care insurance policy designed specifically for care needs. Issue ages typically range from 30 to 79. You can select monthly benefits from $1,500 up to $12,000 (or $15,000 in select states) in $100 increments. Benefit periods are commonly 3 or 6 years, with elimination (waiting) periods of 6, 12, 25, or 52 weeks. Inflation protection options are available to help benefits keep pace with rising care costs. Additional features may include caregiver training benefits, hospice coverage, and the ability to receive care in Canada in approved states. Premiums are paid on an ongoing basis, and the policy is “participating,” meaning it may be eligible for dividends in some cases.

Hybrid LTC: Life Insurance with Long-Term Care Rider (Long-Term Advantage)

This option combines a whole life insurance policy with a long-term care benefit rider. It provides guaranteed coverage for qualified long-term care expenses for a set period (often up to 6 years at the maximum monthly benefit, extendable through dividends). If you never need long-term care—or use only a portion—the policy pays a death benefit to your beneficiaries. Premiums are often structured as level or limited-pay (e.g., 10–20 years), and many hybrids feature guaranteed premiums with no future increases once issued. This “use-it-or-lose-it” protection appeals to those who want lifelong value whether care is needed or not.

Both products include strong spousal and companion discounts (up to 30% when both partners apply and qualify). A premium waiver benefit activates after a qualifying disability period, even if you are not yet receiving long-term care benefits. These policies emphasize flexibility for in-home care, assisted living, nursing facilities, and other qualified services.

Pros and Cons of Northwestern Mutual LTC Insurance

Pros

- Exceptional financial strength: Top-tier ratings across major agencies give policyholders confidence that claims will be paid decades from now.

- High benefit limits: Monthly benefits can reach $12,000–$15,000 in some states—among the highest available.

- Generous couple discounts: Up to 30% spousal or companion discount makes it attractive for married or long-term partners.

- Participating policies: Potential for dividends that can increase benefits or reduce premiums.

- Flexible care options: Covers a wide range of settings, including in-home care, assisted living, and international care in approved cases.

- Strong reputation: Consistent praise for claims-paying ability and customer service from long-term policyholders.

Cons

- Higher premiums: Northwestern Mutual LTC insurance tends to be among the more expensive options in the market.

- Potential rate increases: While historically stable, the company has implemented or announced adjustments on some existing standalone policies due to industry-wide claims experience.

- Strict underwriting: Medical requirements can be rigorous, and not everyone qualifies for the best rates.

- Limited online quoting: Policies are typically sold through Northwestern Mutual financial advisors rather than fully online, which may feel less convenient.

- Not the lowest-cost choice: Buyers seeking the absolute cheapest premiums may find better value elsewhere.

This balance of premium pricing and long-term security is a common theme in reviews of Northwestern Mutual long-term care insurance 2026.

Cost of Northwestern Mutual LTC Insurance in 2026

Northwestern Mutual LTC insurance premiums are generally higher than industry averages, reflecting its strong benefits and financial backing. Exact costs depend on age, health, benefit amount, inflation protection, elimination period, and whether you purchase as an individual or couple.

Illustrative 2026 Examples (approximate, for healthy non-tobacco applicants; actual quotes vary widely):

- A 60-year-old single person seeking $6,000 monthly benefit with 3-year period and 3% compound inflation might pay $200–$350+ per month.

- A 60-year-old couple applying together for similar benefits could see combined premiums reduced by up to 30%, often landing in the $300–$500+ monthly range total.

- Hybrid policies may require higher upfront or limited-pay premiums but lock in rates with no future increases.

Compared with broader industry averages (around $1,175–$1,900 annually for a 60-year-old single with moderate benefits), Northwestern Mutual tends to cost more but may deliver higher lifetime value through larger benefit pools and potential dividends. Factors that increase premiums include higher monthly benefits, longer benefit periods, shorter elimination periods, and stronger inflation riders. Spousal discounts and good health can significantly lower costs.

For more context on industry-wide pricing, see How Much Does Long-Term Care Insurance Cost in 2026?.

Who Is Northwestern Mutual LTC Insurance Best For?

Northwestern Mutual LTC insurance is often a strong fit for:

- Healthy couples in their 50s or early 60s who can qualify for the maximum spousal discount and want high coverage limits.

- Individuals who prioritize financial strength and a mutual company structure that returns value through potential dividends.

- Those seeking flexible, comprehensive protection that covers in-home care, assisted living, and nursing facilities while preserving assets for heirs.

- Buyers comfortable working with a dedicated financial advisor for personalized planning.

It may be less ideal for:

- Budget-conscious buyers seeking the lowest possible premiums.

- Individuals with health conditions that could lead to underwriting declines or higher rates.

- Those who prefer fully online applications and instant quotes.

How Northwestern Mutual LTC Compares to Other Options in 2026?

Northwestern Mutual excels in financial strength and couple-focused features but is premium-priced.

- Vs. New York Life: Similar high ratings and hybrid options; New York Life may offer slightly more flexibility in some hybrid designs.

- Vs. Nationwide: Nationwide often provides more competitive hybrid cash-indemnity options with potentially lower premiums.

- Vs. Mutual of Omaha: Mutual of Omaha is frequently more affordable for standalone coverage while maintaining strong ratings.

Standalone policies like QuietCare suit those who want pure long-term care protection without a life insurance component. Hybrid policies (like Long-Term Advantage) are better if you want a death benefit if care is never needed. For those exploring term vs whole life insurance for seniors as part of broader planning, hybrids can serve as a bridge between protection and legacy goals.

When evaluating carrier reputation, many experts rank Northwestern Mutual among the best insurance companies for seniors 2026 due to its stability and client focus. For Medicare integration discussions, note that long-term care is separate from medicare advantage vs supplement plans 2026, though comprehensive retirement planning often considers both.

How to Apply and Next Steps with Northwestern Mutual?

Applications for Northwestern Mutual LTC insurance are handled through a financial advisor rather than fully online. The process typically includes:

- An initial consultation to assess your needs and goals.

- Medical underwriting (health questionnaire, exam, and records review).

- Custom policy design with your advisor.

Tips for the best outcome: Apply while healthy (ideally in your 50s or early 60s), compare multiple scenarios (standalone vs. hybrid), and ask about current dividend history and rate stability. Always review the policy documents carefully.

Conclusion

Northwestern Mutual LTC insurance in 2026 represents a premium, financially robust choice with high benefit limits, strong couple discounts, and flexible standalone or hybrid options. Its exceptional stability and client-focused features make it especially appealing for couples who prioritize long-term security and asset protection. However, its higher premiums mean it is not the lowest-cost option for every buyer. Carefully compare quotes, weigh your budget and health status, and consider how it fits into your overall retirement plan. This article is for educational purposes only and is not personalized financial or insurance advice. Costs, availability, and policy details can vary. Always consult a licensed insurance professional and review official policy documents before making decisions.

At Retirement Ease Guide we connect you with professional insurance specialists who have helped thousands of retirees find affordable Medicare Advantage plans with the right coverage options for their needs and budget. Get your free, no-obligation personalized Medicare Advantage plan comparison today. Click here to speak with a Medicare plan specialist now.

FAQs

Does Northwestern Mutual still offer standalone long-term care insurance in 2026?

Yes, QuietCare remains available as a traditional standalone policy.

What is the difference between QuietCare and their hybrid LTC policies?

QuietCare is pure long-term care coverage; hybrid policies combine life insurance with a long-term care rider, providing a death benefit if care is not needed.

How much does Northwestern Mutual LTC insurance cost for a 60-year-old couple in 2026?

Costs vary widely but are typically on the higher side—often several hundred dollars per month combined after spousal discounts, depending on benefits chosen.

Does Northwestern Mutual offer spousal discounts on LTC insurance?

Yes, up to 30% for qualifying couples or companions.

Are Northwestern Mutual LTC premiums guaranteed never to increase?

Hybrids often feature guaranteed premiums; standalone policies are guaranteed renewable but may be subject to class-wide increases based on claims experience.

What is the maximum monthly benefit Northwestern Mutual LTC pays?

Up to $12,000–$15,000 per month in some states, depending on the policy and location.

Can I use Northwestern Mutual LTC benefits for in-home care or assisted living?

Yes, benefits can be used for a wide range of qualified services, including in-home care, assisted living, nursing facilities, and more.

How does Northwestern Mutual compare to other long-term care insurance companies?

It excels in financial strength and couple discounts but carries higher premiums than some competitors.

Is Northwestern Mutual a good choice for hybrid life and long-term care insurance?

Yes, for those who want guaranteed coverage plus a potential death benefit and strong company backing.

What should I do if I already have an older Northwestern Mutual LTC policy?

Review your policy with an advisor to understand any recent adjustments, dividend options, or exchange programs that may be available.