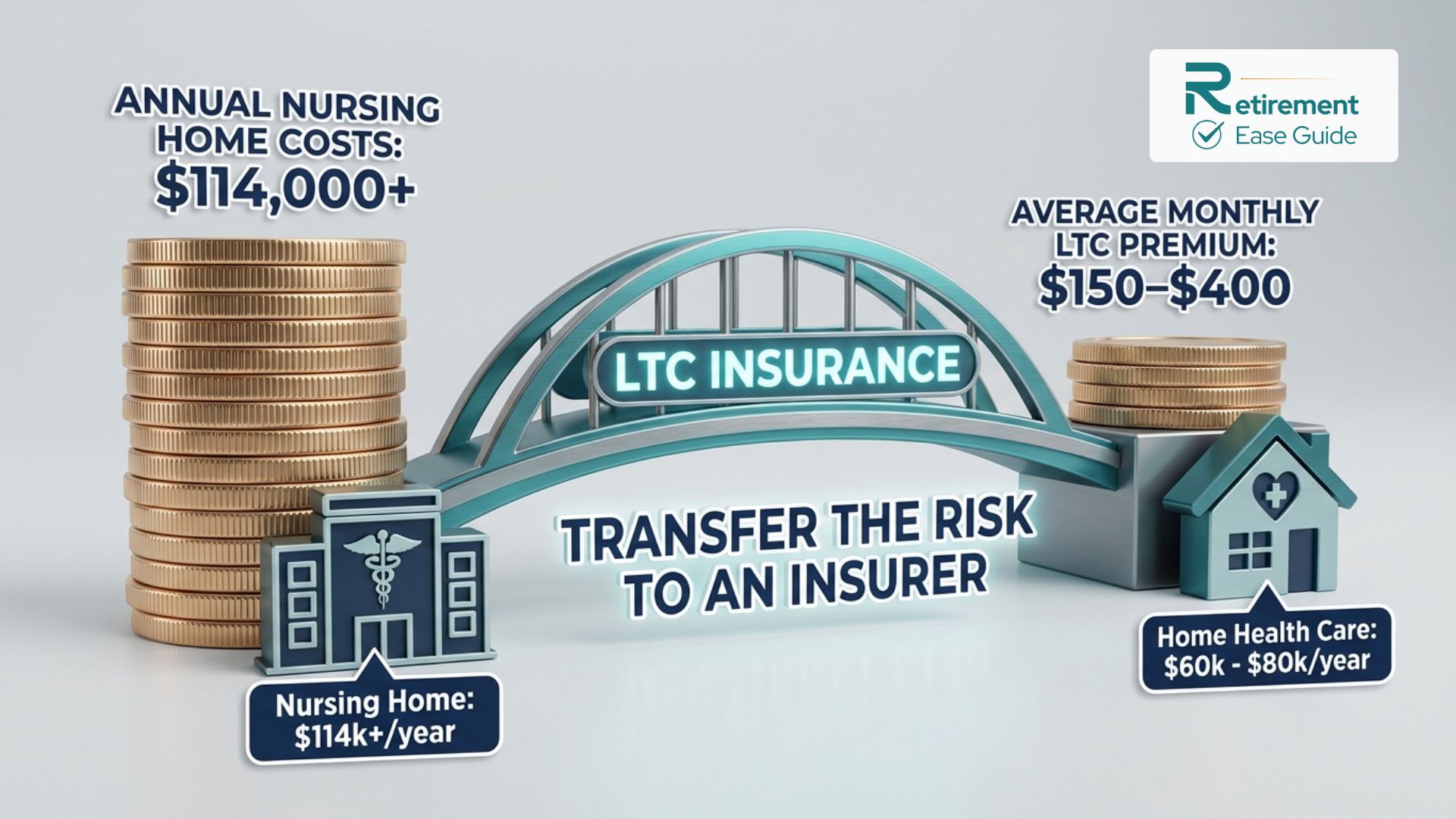

Long-term care needs affect millions of Americans as they age, and the costs of services continue to climb. In 2026, the national median annual cost for a semi-private nursing home room exceeds $114,000, while assisted living averages around $70,000–$75,000 per year and home health aide services often reach $60,000–$80,000 annually. Without planning, these expenses can rapidly deplete retirement savings and place heavy emotional and financial burdens on families.

How much does long-term care insurance cost in 2026 depends on many personal factors, but understanding LTC insurance premiums 2026 helps you make informed decisions. Premiums for traditional policies typically range from about $79 to $533 per month on average, though they vary widely by age, gender, health, and chosen benefits. Planning in 2026 remains critical because buying earlier locks in lower rates, and care costs show no signs of slowing. This guide provides clear, data-based insights drawn from the American Association for Long-Term Care Insurance (AALTCI), Milliman, Genworth/CareScout, and leading carriers to help you and your family prepare with confidence.

Why Long-Term Care Insurance Matters in 2026?

Long-term care (LTC) includes help with daily activities such as bathing, dressing, eating, and mobility—services most people need at some point. According to Milliman’s 2025 Long-Term Care Index (still the latest comprehensive benchmark in early 2026), the projected average lifetime cost of formal paid LTC services for a 65-year-old is about $135,000, with women facing roughly $171,000 and men about $98,000 due to longer life expectancies. These figures assume commercial rates without Medicaid offsets and can range from under $30,000 for short needs to over $660,000 for extended care.

Medicare does not cover most long-term custodial care, only limited skilled nursing in specific situations. Medicaid may step in after you spend down assets, but it often means limited choices and potential reliance on family caregivers. Without insurance, many retirees risk outliving their savings or forcing adult children to sacrifice time, careers, or their own finances. Long-term care insurance for couples 2026 can be especially valuable, offering shared benefits and discounts while protecting joint retirement plans. Planning now provides peace of mind and helps preserve dignity and independence.

Average Cost of Long-Term Care Insurance in 2026

National averages for long-term care insurance cost 2026 reflect policies with an initial $165,000 benefit pool (common benchmark). Monthly premiums generally fall between $79 and $533, translating to roughly $950–$6,400+ annually depending on options.

- Single male: Often lower due to shorter average claim durations.

- Single female: Typically 50–100% higher because women tend to live longer and require more years of care.

- Couples: Combined premiums are usually less than two individual policies thanks to marital discounts (often 25–35% when both apply).

These figures assume “select” health (good but not elite). Preferred health can yield discounts, while substandard health may increase rates or lead to declinations. Actual costs vary significantly by carrier, location, and exact benefits—always request personalized quotes.

Long-Term Care Insurance Costs by Age in 2026

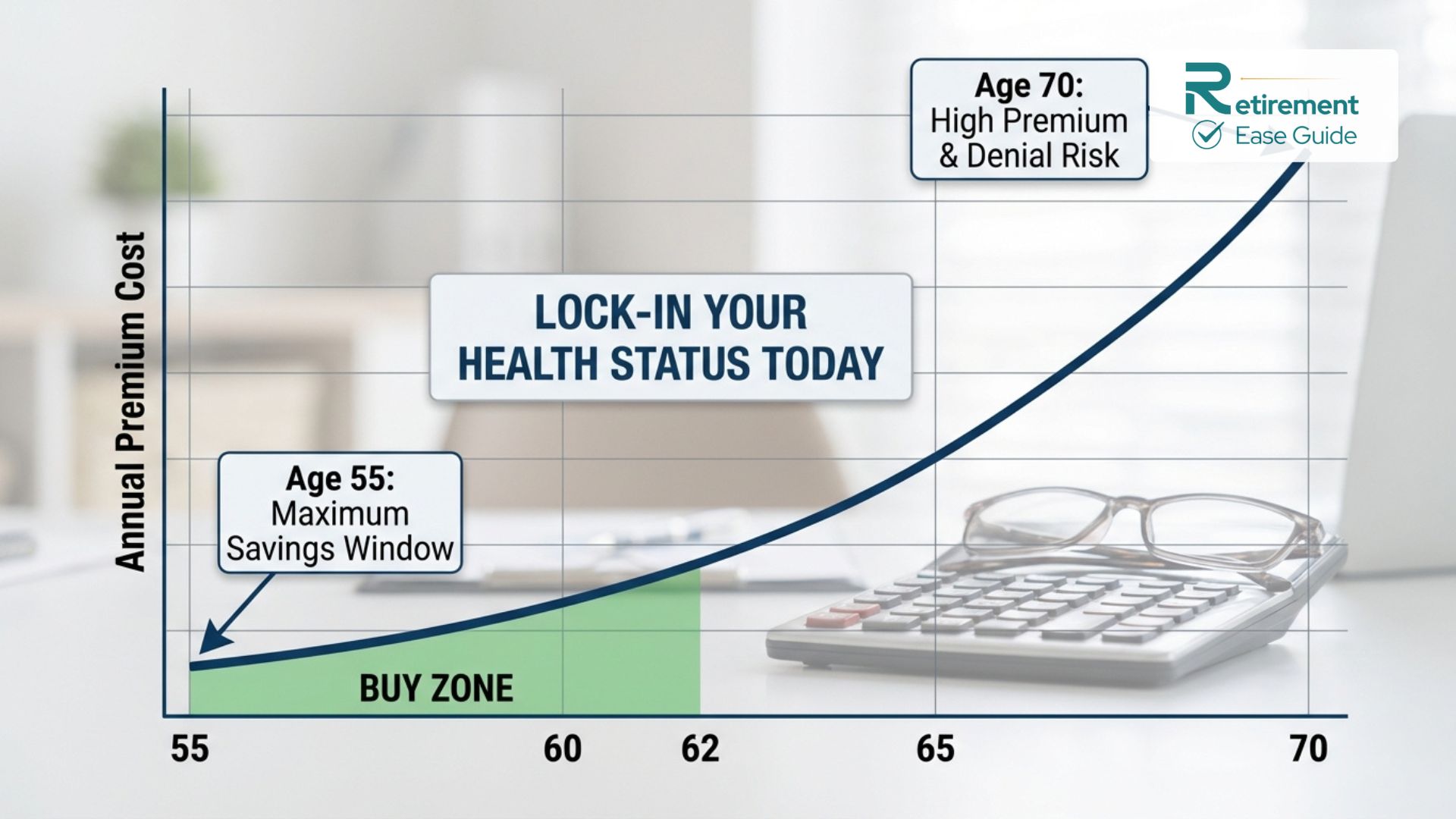

Premiums rise sharply with age because the likelihood of needing care increases. Buying earlier provides substantial savings and more options for inflation protection. Data below draws from AALTCI’s 2025 Price Index (reflecting 2026 market conditions), showing annual premiums for an initial $165,000 benefit pool per person. Figures include variations with compound inflation protection.

At Age 55 (Strongest Savings Window)

- Single Male: $950 (level benefits) to $2,200 (3% inflation) or $3,710 (5% inflation).

- Single Female: $1,500 (level) to $3,750 (3%) or $6,400 (5%).

- Couple (both 55): $2,080 (level) to $5,050 (3%) or $8,575 (5%) combined.

At Age 60

- Single Male: $1,200 (level) to $2,610 (3%) or $3,800 (5%).

- Single Female: $1,900 (level) to $4,550 (3%) or $6,700 (5%).

- Couple (both 60): $2,600 (level) to $5,800 (3%) or $8,700 (5%) combined.

At Age 65 (Common Retirement Planning Point)

- Single Male: $1,750 (level) to $3,280 (3%) or $4,255 (5%).

- Single Female: $2,700 (level) to $5,290 (3%) or $7,225 (5%).

- Couple (both 65): $3,750 (level) to $7,150 (3%) or $9,675 (5%) combined.

For ages 70+, premiums can climb 50–100% or more compared to age 55, with fewer carriers offering robust options and higher denial risks. A 70-year-old might see single premiums starting around $2,000–$4,500+ annually for basic coverage, escalating quickly with inflation riders. The message is clear: long term care insurance rates by age demonstrate that purchasing in your 50s or early 60s can save tens of thousands over a lifetime while securing better benefit growth.

Factors That Affect Long-Term Care Insurance Premiums in 2026

Several key elements drive LTC insurance premiums 2026:

- Age at purchase: The biggest factor—younger buyers lock in lower rates.

- Gender: Women generally pay more due to longer lifespans.

- Health status: Excellent health qualifies for preferred rates; chronic conditions raise costs or limit options.

- Benefit amount and period: Higher daily/monthly benefits or longer coverage (e.g., 3–5 years vs. lifetime) increase premiums.

- Inflation protection: Compound 3% or 5% riders significantly raise upfront costs but preserve purchasing power.

- Elimination period: Longer waits (90 days common) lower premiums since you self-pay initially.

- Partnership policies: These qualify for Medicaid asset protection and may influence design.

- Couples discounts and shared care: Joint policies often reduce costs and allow unused benefits to transfer.

- Policy type: Traditional vs. hybrid (see below).

Location also matters—states with higher care costs or stricter regulations can affect pricing.

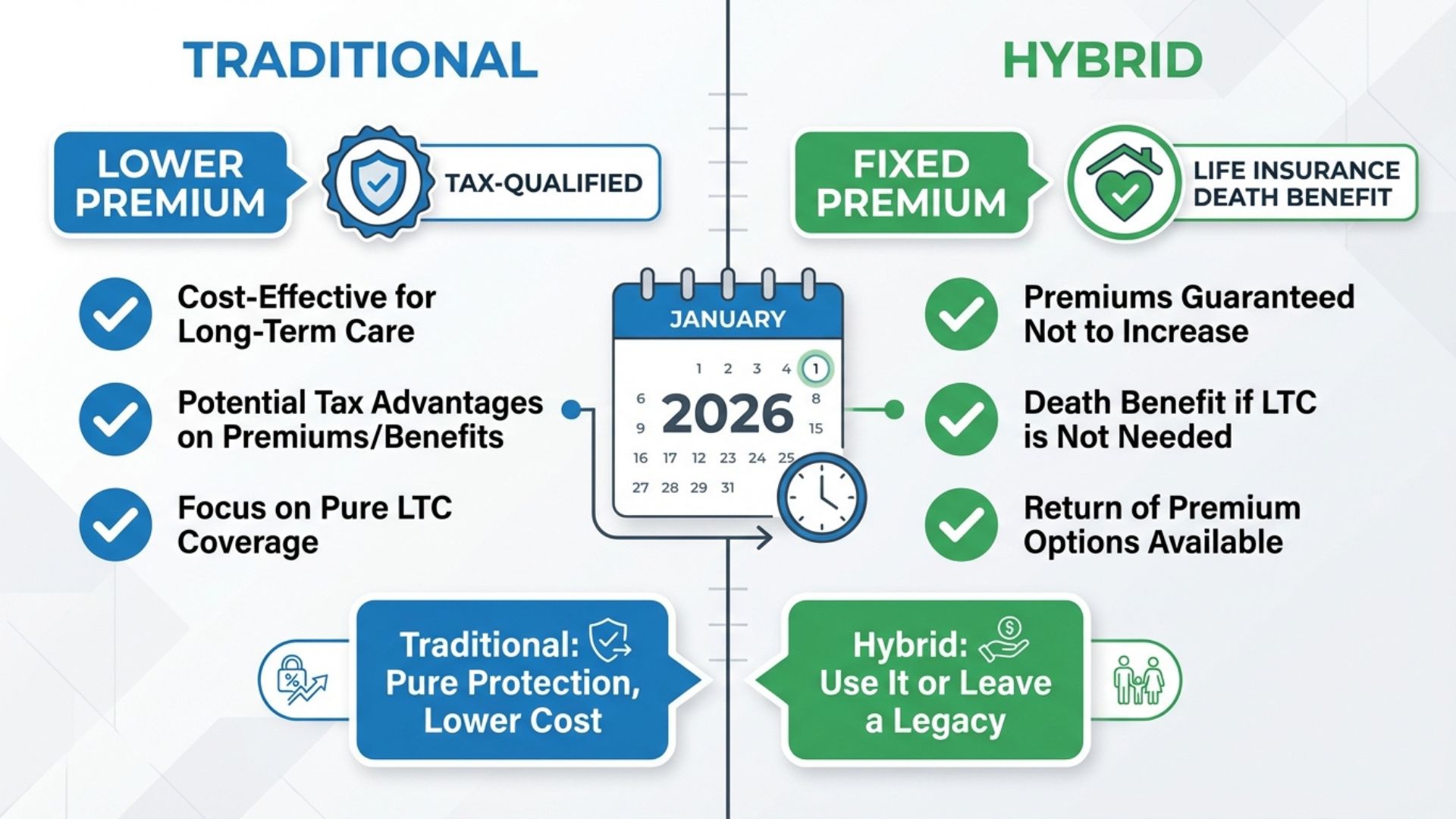

Traditional vs. Hybrid Long-Term Care Insurance Costs

Traditional LTC insurance offers pure protection with flexible benefits but no cash value or death benefit if unused. Premiums are generally lower upfront, though some existing policies face rate increases. Pros include tax-qualified status and Partnership programs. Cons include the risk of premium hikes and “use it or lose it” nature.

Hybrid long-term care insurance links LTC benefits to a life insurance or annuity policy, providing a death benefit if care is never needed. These often feature guaranteed premiums with no future increases and return-of-premium options. However, hybrid long-term care insurance cost is typically 2–4 times higher than traditional for comparable benefits because you pay for the life insurance component. Hybrids appeal to those wanting guaranteed costs and legacy protection.

In 2026, many buyers consider hybrids for predictability amid ongoing traditional policy rate adjustment discussions.

Side-by-Side Comparison Table

The table below shows approximate average annual premiums in 2026 for a policy with an initial $165,000 benefit pool per person (AALTCI benchmark data). “With 3% Inflation” reflects compound growth. Actual quotes will differ.

| Age / Scenario | Single Male (Level / 3% Infl.) | Single Female (Level / 3% Infl.) | Couple Combined (Level / 3% Infl.) | Notes / Best For |

| Age 55 | $950 / $2,200 | $1,500 / $3,750 | $2,080 / $5,050 | Best savings window; strong inflation options |

| Age 60 | $1,200 / $2,610 | $1,900 / $4,550 | $2,600 / $5,800 | Balanced cost & protection |

| Age 65 | $1,750 / $3,280 | $2,700 / $5,290 | $3,750 / $7,150 | Common purchase age; higher premiums |

| Age 70+ (Est.) | $2,500–$4,500+ / Higher | $4,000–$7,000+ / Higher | $5,500–$10,000+ / Higher | Limited options; health critical |

Source: Synthesized from AALTCI 2025 Price Index and industry reports. Premiums assume select health; 90-day elimination; 3–5 year benefit period. Carriers like Mutual of Omaha, New York Life, Northwestern Mutual, and Nationwide are frequent top choices for traditional and hybrid products.

Is Long-Term Care Insurance Worth the Cost in 2026?

Pros: Protects assets, reduces family burden, offers choice in care settings, and provides tax advantages for qualified policies. For couples, shared benefits add flexibility.

Cons: Upfront cost can strain budgets; some policies face rate increases; not everyone qualifies.

Alternatives include self-funding (risky given $135,000+ lifetime averages), Medicaid planning (asset spend-down required), or relying on family. Hybrids blend protection with a death benefit. For many healthy individuals in their 50s–60s, the best long-term care insurance 2026 strikes a balance between affordable premiums and adequate coverage. It is often “worth it” if it preserves independence and legacy.

How to Lower Your Long-Term Care Insurance Costs?

Expert tips to manage average cost of long-term care insurance 2026:

- Buy as early as possible (ideally 50s) for lower locked-in rates.

- Choose a longer elimination period (90 days) to reduce premiums.

- Opt for appropriate (not maximum) daily benefits and benefit periods based on your savings and family support.

- Take advantage of couples discounts and shared-care riders.

- Shop multiple carriers and compare traditional vs. hybrid.

- Maintain excellent health and consider preferred-risk underwriting.

- Explore Partnership policies for asset protection.

- Work with an independent specialist who represents several carriers.

Small adjustments can save thousands while still providing meaningful protection.

Conclusion

How much does long-term care insurance cost in 2026 varies based on your age, health, and choices, but early planning can make coverage far more affordable while safeguarding what matters most. With care costs rising and lifetime needs potentially reaching six figures, understanding LTC insurance premiums 2026 empowers smarter retirement decisions.

Understanding how much long-term care insurance costs in 2026 is the first step toward protecting your retirement savings and your family’s future. With premiums and care costs continuing to rise, personalized guidance is essential to find the right coverage at the best possible rate. Our licensed long-term care insurance specialists have helped thousands of families secure affordable, reliable protection tailored to their needs. Get your free, no-obligation personalized long-term care insurance quote and expert review today. Click here to speak with a long-term care insurance specialist now.

Frequently Asked Questions (FAQ)

What is the average monthly premium for long-term care insurance in 2026?

Expect $79–$533 monthly overall, with many policies falling in the $150–$400 range depending on age and benefits.

Do women pay more for LTC insurance than men?

Yes, typically 50–100% more, primarily because women live longer and have higher lifetime care usage.

What is the best age to buy long-term care insurance?

Ages 55–65 offer the best balance of affordability, availability, and benefit growth options. Earlier is usually cheaper.

How do hybrid policies compare in cost to traditional LTC insurance?

Hybrids usually cost 2–4 times more upfront but provide guaranteed premiums and a death benefit if care is unused.

Does long-term care insurance cover home care?

Most quality policies do, often with flexible benefits for home health aides, adult day care, and assisted living.

Can premiums increase after I buy a policy?

Traditional policies may see increases (some existing ones have faced significant hikes); many hybrids offer guaranteed level premiums.

Is there a discount for couples?

Yes—often 25–35% when both spouses apply together, plus shared benefit features.

What factors most affect my LTC insurance quote?

Age at purchase, health, inflation protection, elimination period, and benefit amount are the primary drivers.