Many retirees feel a sudden shock in their first year on Medicare when medical bills arrive that they never expected. A “$0 premium” Medicare Advantage plan turns out to have high copays for specialist visits, or a simple hospital stay pushes them toward a hefty out-of-pocket maximum. These hidden costs of Medicare plans 2026 can strain fixed retirement incomes and create financial stress at a time when predictability matters most. With healthcare expenses continuing to rise, understanding the true cost of Medicare in 2026 — beyond the headline premium — is more important than ever for protecting your savings and peace of mind.

Why Hidden Costs Matter in Medicare Plans for 2026?

On a fixed income, even modest unexpected expenses add up quickly. Many seniors are drawn to low- or $0-premium plans, only to discover later that copays, coinsurance, network limits, and prior authorization requirements turn “affordable” coverage into a budget buster.

“Low premium” does not always mean low total cost. A plan with a $0 monthly premium might still expose you to thousands in out-of-pocket costs if you need frequent care, expensive prescriptions, or services outside the network. In 2026, with the standard Part B premium rising to $202.90 per month and the Part B deductible increasing to $283, these hidden layers become even more significant for retirees trying to stretch every dollar.

Empathy is important here: you worked hard for your retirement, and the last thing you want is a surprise medical bill eroding your security. The good news is that with careful planning and the right questions, you can minimize or avoid many of these unexpected Medicare expenses.

The Biggest Hidden Costs of Medicare Advantage Plans in 2026

Medicare Advantage (Part C) plans bundle Parts A, B, and usually D, often with extra benefits. However, they frequently come with cost-sharing mechanisms that can catch enrollees off guard.

High Out-of-Pocket Maximums

Every Medicare Advantage plan has an annual out-of-pocket maximum (MOOP) for in-network services covered under Parts A and B. In 2026, the federal limit is $9,250 (down slightly from $9,350 in 2025), but many plans set their MOOP lower — or, in practice, members reach high amounts before hitting the cap. Once you reach the MOOP, the plan pays 100% of covered services for the rest of the year, but getting there can still mean significant spending on copays and coinsurance.

Copays and Coinsurance on Services

Instead of Original Medicare’s 20% coinsurance after the deductible, Medicare Advantage plans typically charge fixed copays (e.g., $20–$50 for a primary care visit, $100+ for specialists, or daily copays for hospital stays). These can accumulate rapidly during a serious illness or ongoing treatment. Some plans shift to coinsurance on certain services, adding unpredictability.

Prior Authorization Denials and Delays

Many plans require prior authorization for surgeries, advanced imaging, certain medications, or therapies. Delays or denials can lead to postponed care, higher out-of-network costs if you seek alternatives, or outright uncovered expenses. Appeals take time and effort, during which you might pay out of pocket.

Network Restrictions & Out-of-Network Costs

Medicare Advantage plans usually limit you to in-network providers (HMO or PPO models). Seeing an out-of-network doctor or hospital can mean full responsibility for the bill or much higher cost-sharing. Networks can change annually, so your trusted physician might no longer be covered in 2026.

Prescription Drug Costs (Donut Hole / Coverage Gap)

The classic “donut hole” has been eliminated. In 2026, after any plan deductible (up to $615 maximum), you typically pay 25% of covered drug costs until your out-of-pocket spending on prescriptions reaches $2,100. At that point, you enter catastrophic coverage with $0 cost-sharing for the rest of the year on covered Part D drugs. However, the deductible and 25% phase can still create meaningful hidden costs Medicare Advantage 2026 if you take expensive medications.

Extra Benefits That Aren’t Truly Free

Dental, vision, hearing, gym memberships, or transportation allowances sound appealing, but they often come with limits, copays, annual maximums, or network restrictions. A “free” dental cleaning might still leave you paying 50% for major work, and over-the-counter allowances may not cover what you actually need.

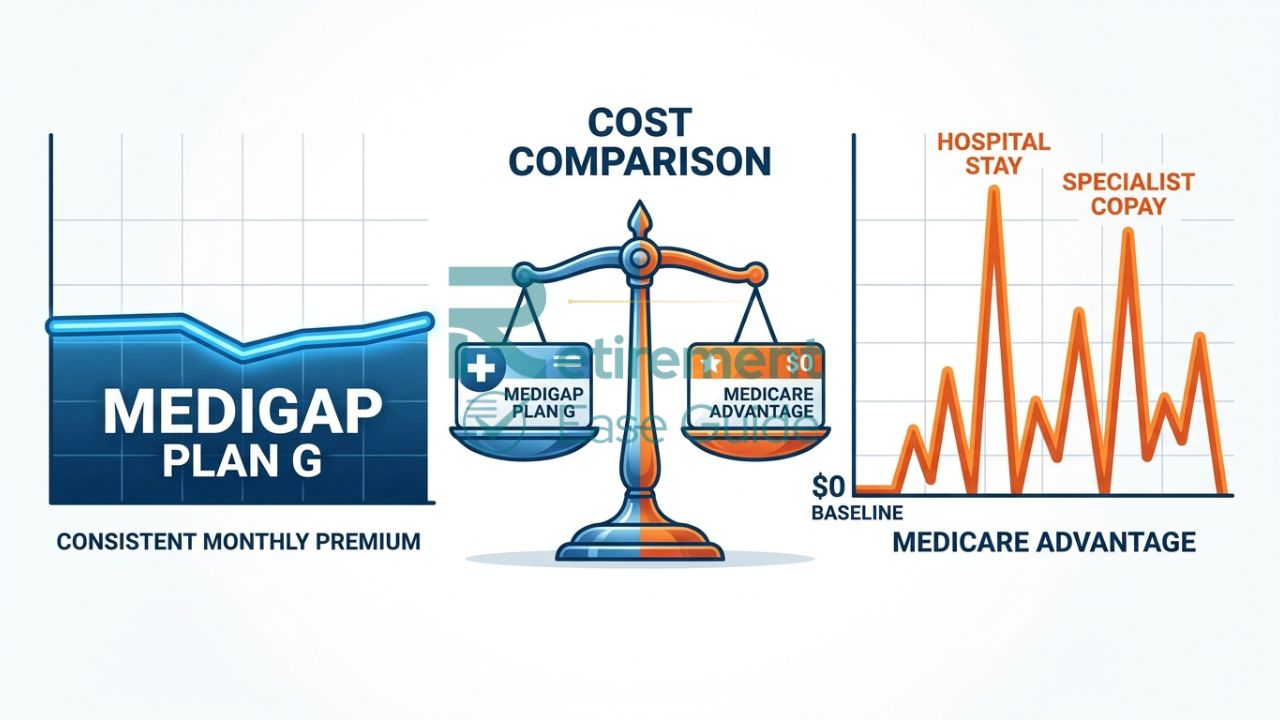

Hidden Costs of Original Medicare + Medigap in 2026

Original Medicare (Parts A and B) offers broad provider choice but leaves significant gaps that Medigap helps fill.

Part B Premium

Most beneficiaries pay the standard Part B premium of $202.90 per month in 2026 (up $17.90 from 2025). Higher-income individuals pay more via IRMAA surcharges based on 2024 tax returns. This premium is due every month regardless of whether you use services.

Part B Deductible

You pay the first $283 of approved Part B services each year before coverage begins.

Medigap Premium Increases

Medigap (Medicare Supplement) premiums vary by plan, insurer, age, location, and rating method (attained-age, issue-age, or community-rated). Many plans see annual increases due to medical inflation and claims experience. Plan G remains popular because it covers most gaps after the Part B deductible, but premiums can rise over time.

Excess Charges (if no Medigap Plan G or F)

If a provider does not accept Medicare assignment, they can charge up to 15% above the approved amount (excess charges). Plans like G or F cover these; others may leave you responsible.

Other Often-Overlooked Medicare Expenses in 2026

- Dental, Vision, and Hearing: Original Medicare covers these minimally. Medicare Advantage extras often have caps (e.g., $1,500–$3,000 annual dental maximum) and copays, leaving substantial costs for dentures, implants, glasses, or hearing aids.

- Transportation to Medical Appointments: Ride-sharing or ambulance costs (non-emergency) may not be fully covered or could have limits.

- Home Health Care Limitations: Medicare has strict criteria; extended or custodial care is usually not covered.

- Inflation Adjustments and Rate Changes: Premiums, deductibles, and copays adjust yearly. Plans may also change benefits, networks, or formularies during the Annual Notice of Change (ANOC) period.

Working with a knowledgeable Medicare agent can help uncover these details before you enroll.

Side-by-Side Cost Comparison Table: Medicare Advantage vs Original Medicare + Medigap

Here’s a realistic 2026 scenario for a healthy 68-year-old in a typical urban area (costs are illustrative averages and vary significantly by plan, ZIP code, and usage):

| Cost Element | Medicare Advantage (Typical $0 Premium Plan) | Original Medicare + Medigap Plan G |

| Monthly Premium (Part B + Plan/Medigap) | $202.90 (Part B) + $0 plan premium | $202.90 (Part B) + $120–$200 Medigap |

| Annual Deductible | Varies ($0–$500 common) | $283 (Part B) — covered by Medigap after |

| Doctor Visit Copay/Coinsurance | $10–$50 copay per visit | $0 after deductible (Medigap covers) |

| Hospital Stay (e.g., 5 days) | Daily copays until MOOP | $0 after Part A deductible (Medigap covers) |

| Out-of-Pocket Maximum (Medical) | Up to $9,250 (in-network) | No limit needed (Medigap fills gaps) |

| Part D Drug OOP Cap | $2,100 | Separate Part D plan: up to $2,100 |

| Network Flexibility | Limited to network | Any Medicare-accepting provider |

| Prior Authorization | Often required | Rarely required |

Key takeaway: Medicare Advantage may save on premiums but can cost more with heavy usage. Medigap offers predictability at higher monthly cost. Always run your specific medications and doctors through Medicare.gov’s Plan Finder.

Hidden Cost Checklist: Questions to Ask Before Enrolling

Use this checklist to protect yourself:

- Does my doctor and hospital stay in-network for 2026?

- What are the copays for primary care, specialists, hospital days, and emergency care?

- Which services require prior authorization, and what is the approval process?

- What is the plan’s actual out-of-pocket maximum, and how likely am I to reach it?

- How does the drug formulary cover my prescriptions, including tiers and restrictions?

- What are the limits on dental, vision, and hearing benefits?

- Are there any “giveback” Part B premium reductions, and what trade-offs come with them?

- How have this plan’s networks or benefits changed from last year?

- What will my total estimated annual costs be with my current health needs?

A licensed agent can help answer these with your specific data.

How to Avoid or Minimize Hidden Medicare Costs in 2026?

- Compare plans using Medicare.gov’s Plan Finder with your actual doctors and prescriptions.

- Review the Annual Notice of Change (ANOC) every fall.

- Consider your health trajectory — frequent care may favor Medigap; occasional care may suit Medicare Advantage.

- Check for plans with lower MOOPs or generous Part B givebacks, but verify trade-offs.

- Work with an independent Medicare specialist who can shop multiple carriers without bias.

- Budget for the Part B premium and deductible even in “$0 premium” plans.

- Appeal denials promptly and document everything.

Plan availability, benefits, and costs vary significantly by county and ZIP code. What works for your neighbor may not work for you.

Related Medicare Planning Resources

For deeper guidance, explore these helpful articles from our site:

Learn more in our guide to the Best Medicare Advantage Plans in 2026.

Compare overall options with the Best Affordable Health Insurance for Retirees in 2026.

If you live in the Sunshine State, connect with experts through Medicare agents near me in Florida.

Conclusion

Understanding the hidden costs of Medicare plans in 2026 can protect your retirement savings from unexpected medical expenses. Many seniors end up paying far more than expected because they didn’t fully understand the fine print. At Retirement Ease Guide we connect you with professional Medicare plan specialists have helped thousands of retirees choose plans with transparent, predictable costs that truly fit their budget. Get your free, no-obligation personalized Medicare plan review and hidden cost analysis today. Click here to speak with a Medicare plan specialist now.

Frequently Asked Questions (FAQ)

What are the main hidden costs of Medicare Advantage 2026?

Copays, coinsurance, prior authorization delays, network restrictions, and reaching the out-of-pocket maximum before coverage becomes “free.”

How much is the Part B premium in 2026?

The standard premium is $202.90 per month, with higher amounts for those with elevated income via IRMAA.

Is there still a donut hole in 2026?

No — the coverage gap has been eliminated. You pay up to 25% on drugs until reaching the $2,100 out-of-pocket cap for Part D, then catastrophic coverage applies.

Does Medigap have hidden costs?

Mainly potential premium increases over time and the fact that you still need a separate Part D plan.

Can I avoid network restrictions costs?

Yes — by choosing Original Medicare + Medigap or a Medicare Advantage PPO with strong out-of-network coverage (at higher cost-sharing).

Are extra benefits in Medicare Advantage truly free?

They often have limits, copays, or network rules that reduce their real-world value.

What is the Medicare Advantage out-of-pocket maximum in 2026?

The federal cap is $9,250 for in-network services, but individual plans may set lower limits.

Will my costs change if my health worsens in 2026?

Possibly — higher utilization can push you toward the MOOP faster in Medicare Advantage, while Medigap offers more stable gap coverage.

How can I find my true cost of Medicare in 2026?

Use Medicare.gov, review plan documents, and consult a licensed agent for personalized estimates.

Is it better to have Medicare Advantage or Medigap in 2026?

It depends on your location, doctors, budget, and expected healthcare use. Many retirees benefit from professional guidance.