Retirement should be a time of enjoyment and relaxation, yet rising healthcare costs often create significant worry for seniors living on fixed incomes. With the standard Medicare Part B premium rising to $202.90 per month in 2026 (an increase of $17.90 from 2025) and out-of-pocket expenses for care continuing to climb, many retirees and their adult children seek reliable ways to manage costs without sacrificing necessary coverage.

The best affordable health insurance for retirees in 2026 balances low or $0 additional premiums, manageable out-of-pocket maximums, and valuable extra benefits. Options range from $0 premium Medicare Advantage plans 2026 that bundle extras like dental and vision to Medigap supplements for more predictable spending. Understanding these choices helps protect your savings and provides peace of mind during your golden years. This guide draws on the latest 2026 data from CMS, Medicare.gov, and independent analyses to offer clear, practical insights.

Health Insurance Challenges for Retirees in 2026

Many retirees face higher healthcare expenses at a time when income is often limited to Social Security, pensions, or savings. Medicare provides a strong foundation at age 65, but it has gaps. Original Medicare (Parts A and B) covers hospital and medical services but leaves you responsible for deductibles, coinsurance, and services like routine dental, vision, and hearing—costs that add up quickly.

In 2026, the Part B deductible rises to $283, and without supplemental coverage, you could face 20% coinsurance on many outpatient services with no annual cap. Inflation and rising care costs (such as nursing home stays averaging over $114,000 annually in some reports) compound the issue. Early retirees under 65 encounter even greater hurdles, as they must bridge coverage until Medicare eligibility, often turning to ACA Marketplace plans or COBRA.

Affordable health insurance for retirees 2026 requires weighing monthly premiums against potential out-of-pocket costs, network access, and your specific health needs. Location, health status, and prescription drugs all influence total expenses, so personalized comparison is essential.

Main Affordable Health Insurance Options for Retirees in 2026

Retirees generally have several pathways depending on age and income.

Medicare Advantage (Part C) Plans

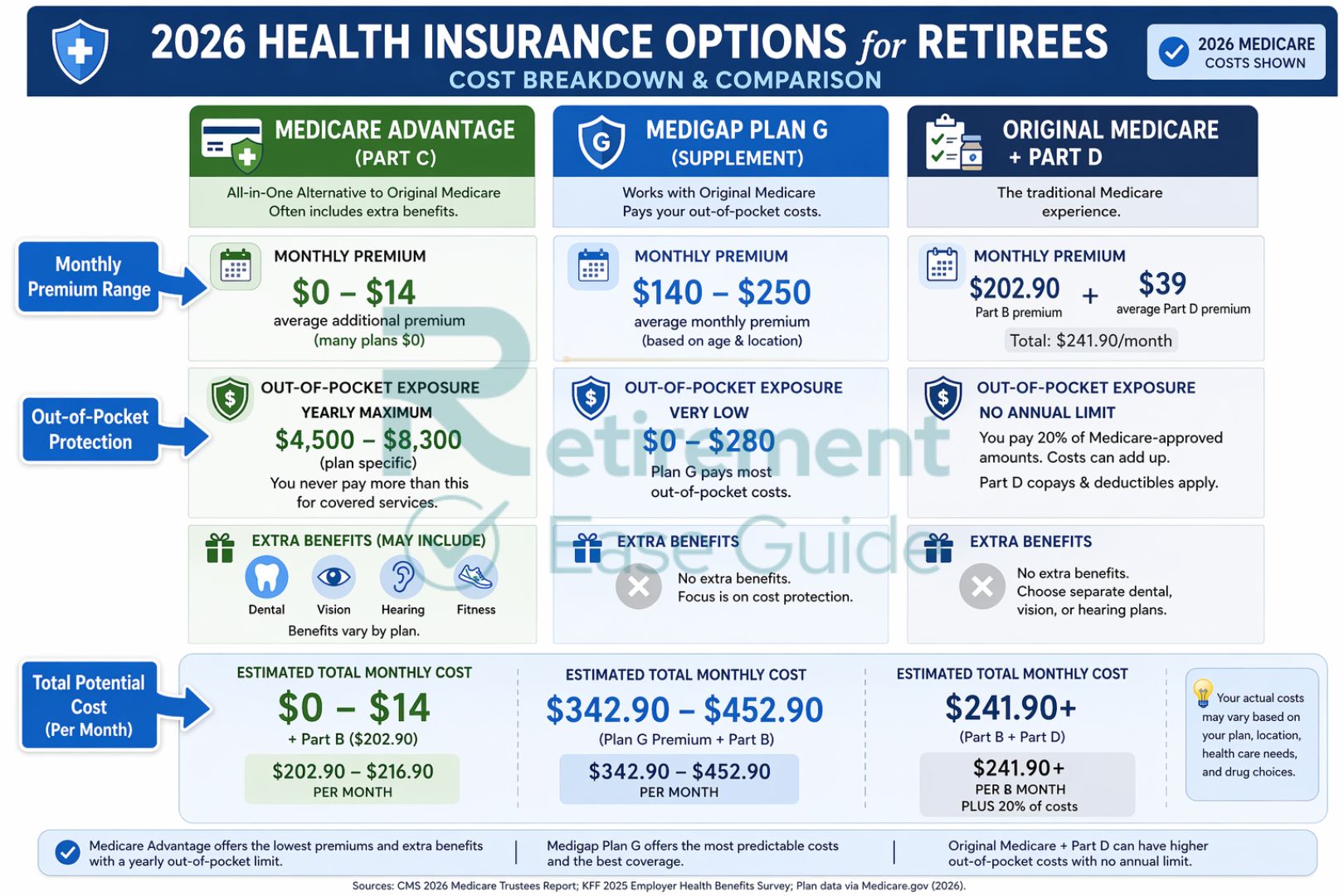

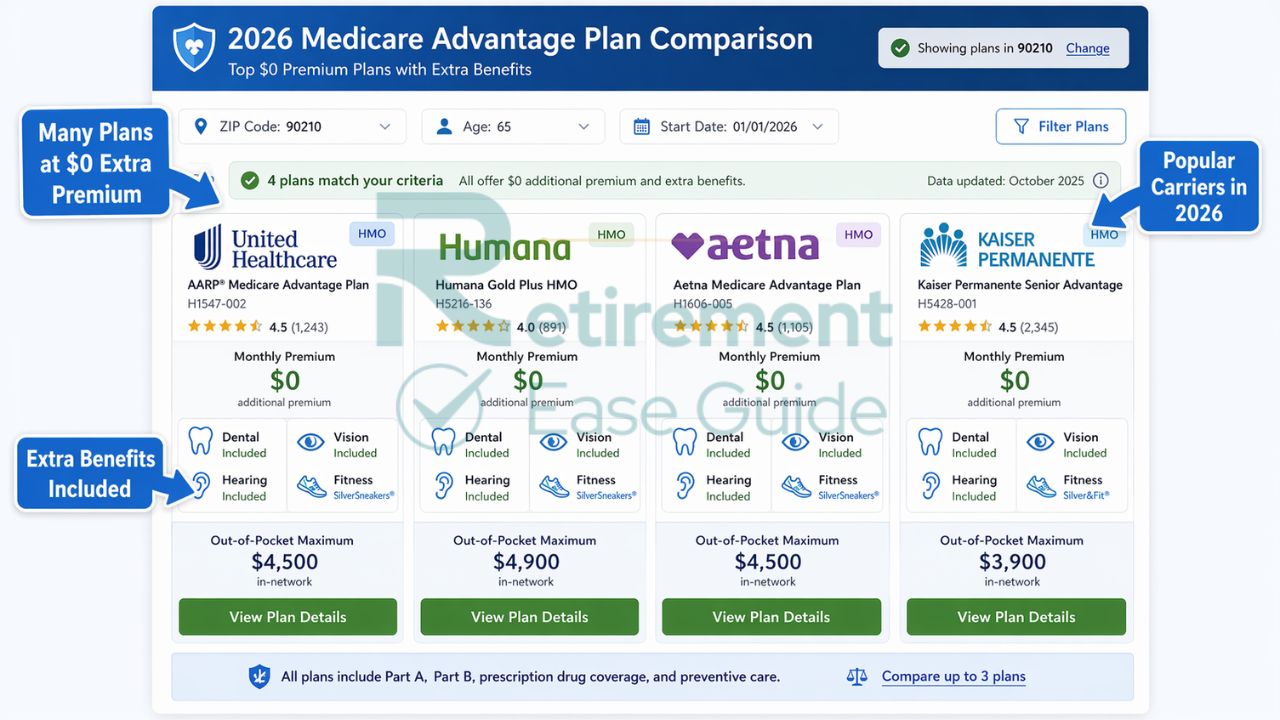

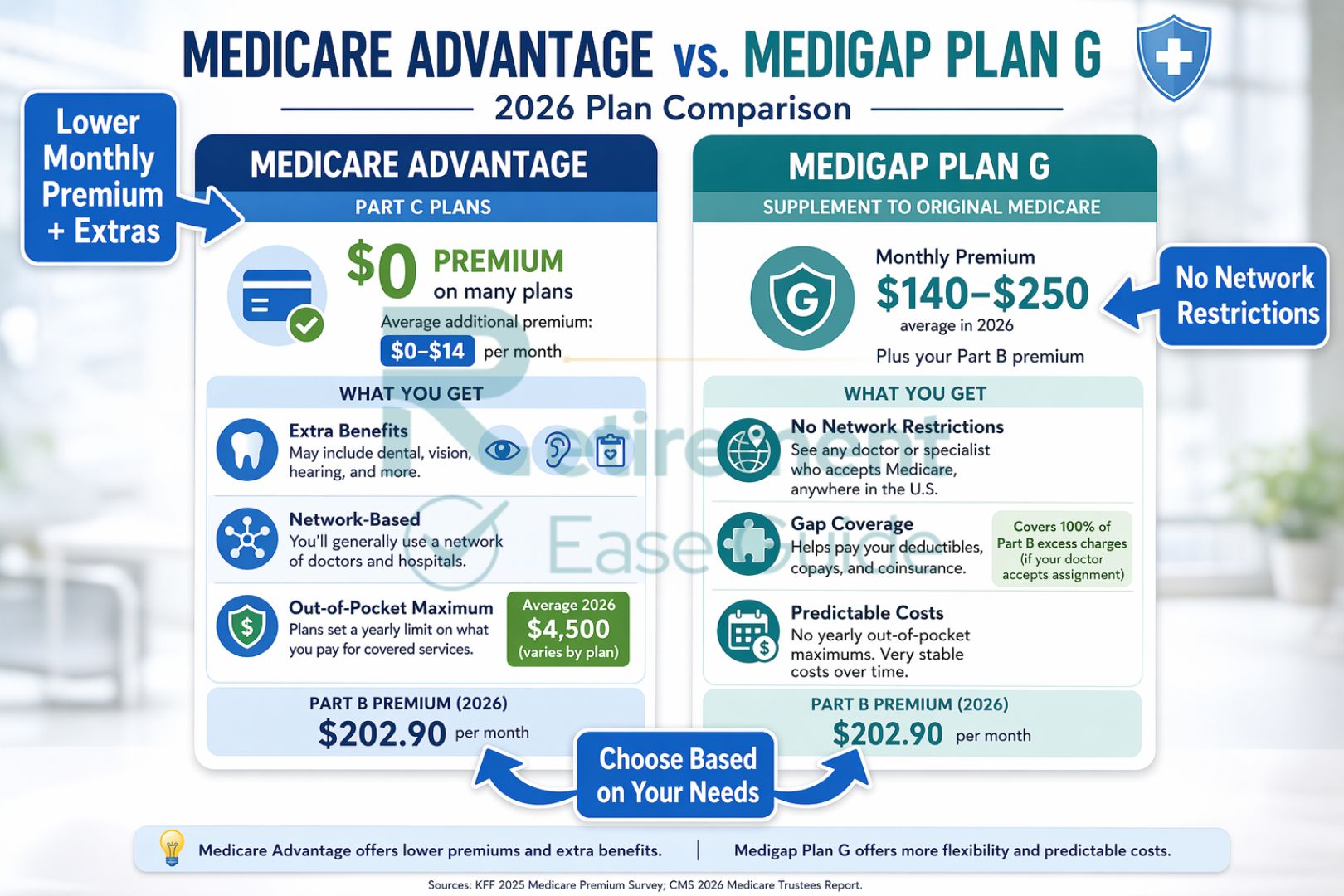

These private plans approved by Medicare combine Parts A and B (and usually Part D) into one package. Many feature $0 premium Medicare Advantage plans 2026 beyond the Part B premium, plus extras not covered by Original Medicare. Average additional MA premiums remain low, around $11–$14 monthly in national estimates, with about two-thirds of plans offering $0 additional premium. In-network out-of-pocket maximums provide a spending cap (up to $9,250 or higher depending on plan specifics in 2026 data trends).

Medigap (Medicare Supplement) Plans

These standardized policies work with Original Medicare to cover gaps like deductibles and coinsurance. They offer predictable costs with no network restrictions in most cases. Premiums typically range from $100–$300+ monthly depending on plan letter (e.g., Plan G or N), age, gender, and location, but they eliminate most surprise bills.

Original Medicare + Part D

You pay the Part B premium ($202.90 standard) plus a separate Part D drug plan (national base around $39). This provides broad provider access but requires managing deductibles, coinsurance, and separate drug coverage. No overall out-of-pocket cap exists without additional protection.

Marketplace / ACA Plans (for Early Retirees Under 65)

If you retire before 65 and lose employer coverage, the Health Insurance Marketplace offers subsidized plans. Premium tax credits can reduce costs significantly, sometimes to $0 for eligible lower-income individuals. These plans must cover essential benefits and are available year-round with qualifying events.

Medicaid or Medicare Savings Programs (for Low-Income Retirees)

Qualifying retirees may receive help with premiums, deductibles, or full coverage through state Medicaid or Medicare Savings Programs, making healthcare essentially free or very low-cost.

Best Affordable Health Insurance for Retirees in 2026

“Best” depends on your health, budget, doctors, and location, but several carriers consistently stand out for value in 2026 reviews.

Best Overall Affordable Option

Kaiser Permanente often ranks highly for integrated care and affordability in its service areas (primarily West Coast and select regions). Its Medicare Advantage plans frequently combine low or $0 premiums with coordinated care, strong chronic condition management, and included extras.

Best $0 Premium Medicare Advantage Plans

UnitedHealthcare (including AARP plans), Humana, Aetna, and Cigna lead in availability of $0 additional premium options across many counties. These plans typically include Part D and extras like dental cleanings, vision allowances, hearing aids, and fitness programs (e.g., SilverSneakers). UnitedHealthcare and Humana offer broad national reach, while Aetna emphasizes wellness and low copays in many markets.

Best for Predictable Out-of-Pocket Costs (Medigap)

Medigap Plan G or N (sold by carriers like Mutual of Omaha, UnitedHealthcare, or Blue Cross Blue Shield affiliates) provides the most predictable spending. Plan G covers most gaps after the Part B deductible, while Plan N offers lower premiums with small copays for office visits and ER. Average premiums for a 65-year-old often fall in the $140–$250 range depending on the state and insurer.

Best for Extra Benefits (Dental, Vision, Hearing, Gym)

Medicare Advantage plans from Humana and Aetna frequently excel here, offering robust allowances for routine dental (fillings, crowns), vision exams/eyewear, hearing aids, and over-the-counter allowances. Many include gym memberships or transportation to appointments—benefits not available with Original Medicare alone.

Best for Early Retirees (Under 65)

ACA Marketplace plans through HealthCare.gov remain the primary option, with subsidies making coverage more affordable. Some states offer additional programs, and short-term or COBRA extensions can serve as bridges. Once you turn 65, transitioning to Medicare is straightforward.

Other strong carriers include Blue Cross Blue Shield affiliates for regional strength and Devoted Health for high member satisfaction in its markets.

Medicare Advantage vs Medigap: Which Is More Affordable in 2026?

This common comparison depends on your priorities:

- Monthly Premiums: Medicare Advantage often wins with many $0 additional premiums (you still pay Part B $202.90). Medigap adds $100–$300+ on top of Part B.

- Out-of-Pocket Maximums: MA plans cap in-network spending (trending around $5,900–$9,850 median/max in 2026 analyses). Medigap with Original Medicare has no cap but covers most cost-sharing, leading to very low unexpected bills if you use providers that accept Medicare.

- Network Restrictions: MA usually requires in-network providers (HMOs stricter than PPOs). Medigap offers freedom to see any Medicare-accepting provider nationwide.

- Extra Benefits: MA typically includes dental, vision, hearing, and more. Medigap focuses on filling Original Medicare gaps without extras.

- Total Potential Costs: On a tight budget with average health, a $0 premium MA plan may feel more affordable upfront. For frequent care or travel, Medigap often provides better long-term predictability despite higher monthly premiums.

Many retirees choose MA for value and extras, while others prefer Medigap for flexibility and peace of mind. A Medicare Advantage vs Medigap cost 2026 analysis in your ZIP code is the best way to decide.

Side-by-Side Comparison Table of the Top Affordable Options

The table below illustrates representative 2026 costs and features (national trends; actual amounts vary significantly by location and health—use Medicare.gov for precise quotes).

| Option / Carrier Example | Best For | Monthly Premium Range (Beyond Part B Where Applicable) | Out-of-Pocket Max / Exposure | Key Benefits | Drawbacks |

| Medicare Advantage (e.g., UnitedHealthcare, Humana, Aetna) | $0 premium & extras | $0 – $14 average additional | Up to ~$9,250 in-network | Dental, vision, hearing, fitness, Part D | Network restrictions, prior auth |

| Medigap Plan G (various carriers) | Predictable costs | $140 – $250+ (age 65 average) | Low (after Part B deductible) | Broad provider access, gap coverage | Higher monthly premium, no extras |

| Original Medicare + Part D | Maximum provider choice | Part B $202.90 + Part D ~$39 base | No annual cap | Any Medicare provider | Higher potential out-of-pocket |

| Kaiser Permanente MA | Integrated affordable care | Often $0 additional | Plan-specific cap | Coordinated care, extras included | Limited service areas |

| ACA Marketplace (under 65) | Early retirees | Varies; often $0–low with subsidies | Plan-specific (often lower) | Essential benefits, subsidies | Income-based eligibility, annual changes |

Data reflects 2026 CMS trends and independent reviews. Premiums and MOOP can differ by county and individual factors.

How to Choose the Most Affordable Health Insurance as a Retiree in 2026?

Follow this expert checklist:

- Assess your budget — Factor in the Part B premium and any additional costs.

- Review your health needs and current medications.

- Confirm your preferred doctors and hospitals are in-network (for MA) or accept Medicare (for Medigap).

- Consider prescription drug coverage and formulary.

- Think about travel or snowbird plans — Medigap or PPO-style MA may suit better.

- Evaluate extras if dental, vision, or hearing matter to you.

- Check eligibility for help programs if income is limited.

[Link to “How to Choose a Medicare Plan in 2026”] for more details. The Annual Enrollment Period (Oct 15–Dec 7) is the ideal time to compare and switch.

Tips to Lower Your Health Insurance Costs in Retirement

- Enroll in a $0 premium Medicare Advantage plan if it fits your needs.

- Shop multiple carriers and plans each year using Medicare.gov’s Plan Finder.

- Maintain healthy habits to potentially qualify for better rates or avoid penalties.

- Explore Medicare Savings Programs or Extra Help for Part D if eligible.

- Consider a high-deductible Medigap option or longer elimination periods where available.

- Bundle with other retiree benefits or spousal coverage when possible.

- Work with an independent licensed advisor who can compare options across carriers without bias.

Small choices can lead to meaningful annual savings while preserving access to quality care.

Conclusion

The best affordable health insurance for retirees in 2026 combines smart planning with options that match your health, budget, and lifestyle. Whether a low-premium Medicare Advantage plan with extras or a Medigap policy for predictability, the right choice helps safeguard your retirement while addressing cheapest health insurance for seniors 2026 concerns and low premium health insurance for retirees.

Finding the best affordable health insurance for retirees in 2026 can significantly protect your retirement savings and provide peace of mind during your golden years. With so many options and costs varying by location and health status, personalized expert guidance makes all the difference. Our licensed Medicare and health insurance specialists have helped thousands of retirees secure the right coverage at the lowest possible cost. Get your free, no-obligation personalized health insurance review for retirees today. Click here to speak with a Medicare plan specialist now.

Frequently Asked Questions (FAQ)

What is the cheapest health insurance for retirees in 2026?

Many $0 premium Medicare Advantage plans offer the lowest upfront cost for those 65+, though total value depends on usage. For early retirees, subsidized ACA plans can be very low or $0.

Is Medicare Advantage really free?

Most charge no additional premium beyond the standard Part B ($202.90 in 2026), but you may have copays and a maximum out-of-pocket limit.

How much does Medigap cost in 2026?

Average premiums range from about $100–$300 monthly, varying by plan type (G or N common), age, gender, and state.

Are $0 premium Medicare Advantage plans 2026 a good deal?

They often provide strong value with extras, but review networks, drug coverage, and MOOP carefully.

What are the best Medicare plans for retirees on a budget?

Kaiser, UnitedHealthcare, Humana, and Aetna frequently offer competitive affordable options with good reviews.

How do Medicare Advantage vs Medigap costs compare in 2026?

MA tends to have lower monthly premiums and caps on spending but with networks; Medigap has higher premiums but greater flexibility and predictability.

Can early retirees under 65 find affordable coverage?

Yes—ACA Marketplace plans with subsidies are the main route, sometimes reducing premiums dramatically.

Does location affect affordable health insurance for retirees?

Yes—plan availability, premiums, and provider networks vary significantly by county and state.