As you enter or navigate your retirement years, the thought of leaving behind unexpected financial burdens for your loved ones can weigh heavily on your mind. Funeral costs continue to rise with inflation, and many families face thousands in final expenses at an already emotional time. Best senior life insurance plans in 2026 provide a compassionate solution—offering peace of mind that your family won’t struggle with burial costs, medical bills, or other end-of-life expenses. With options ranging from simple final expense insurance 2026 to guaranteed issue life insurance for seniors and no medical exam life insurance for seniors, there’s coverage tailored for adults aged 50 and beyond.

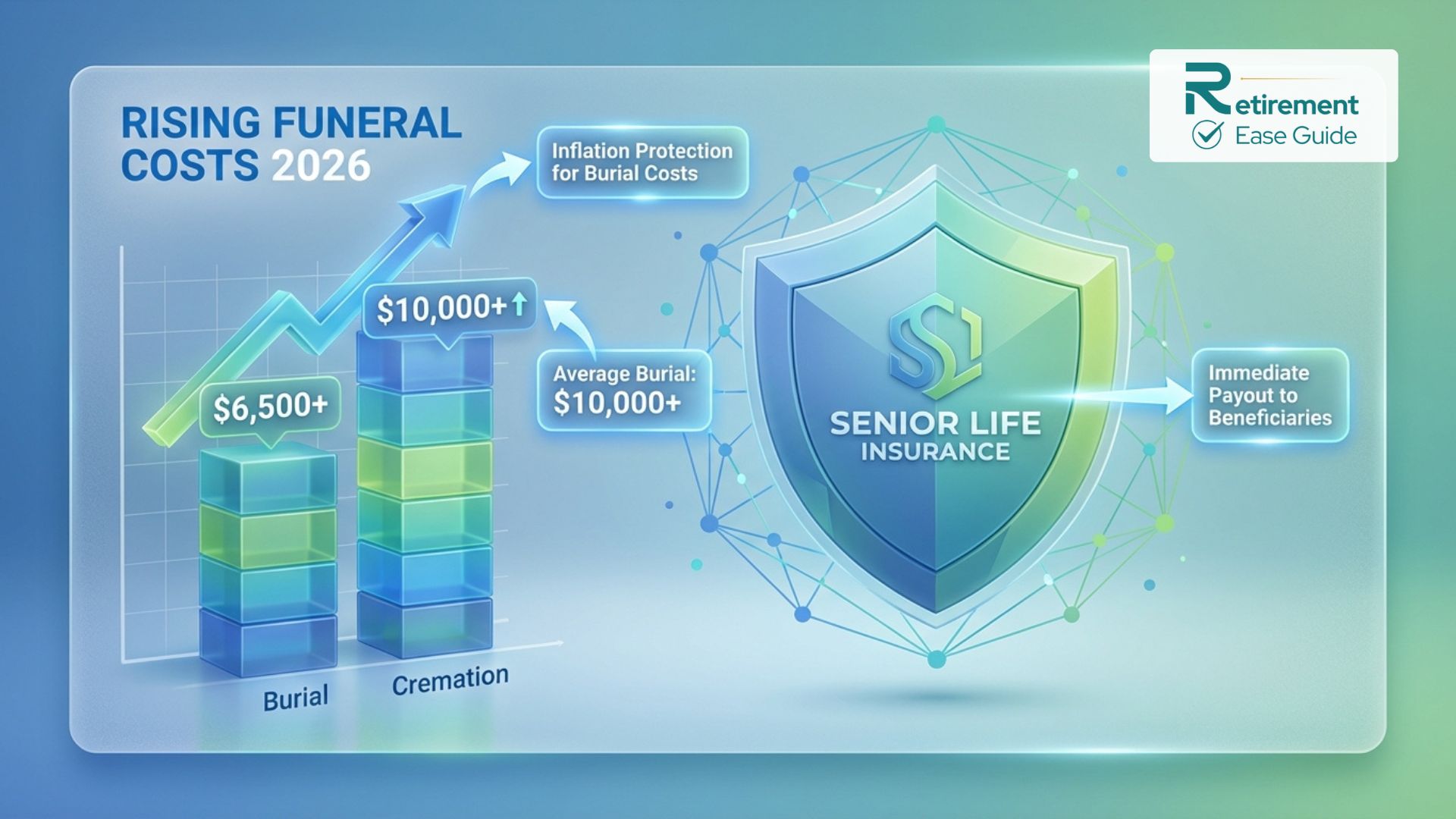

In 2026, senior life insurance remains accessible and affordable for most, with many carriers offering fixed premiums that never increase and benefits that can help cover the national median funeral costs (around $8,300 for a traditional burial with viewing or $6,280 for cremation with services, though totals often reach $10,000+ when including additional fees). Whether you seek affordable senior life insurance plans, burial insurance 2026, or senior whole life insurance with potential cash value, understanding your options empowers you to protect those you love.

Why Seniors Need Life Insurance in 2026?

Life insurance isn’t just for young families raising children—it serves a vital role for seniors too. At this stage of life, the focus shifts from income replacement to covering final expenses and leaving a legacy.

- Rising funeral and burial costs: The median cost of a funeral with burial and viewing hovers around $8,300 nationally, while cremation services average about $6,280. Adding cemetery plots, vaults, headstones, or transportation can push totals significantly higher. Inflation has driven these expenses upward in recent years.

- Avoiding burden on family: Without coverage, loved ones may face credit card debt, outstanding medical bills, or loans alongside grief. Even modest policies prevent this stress.

- Leaving a legacy or inheritance: Some seniors use permanent policies to gift funds for grandchildren’s education, charitable causes, or simply to ease financial transitions.

- Inflation protection: Fixed-premium whole life or final expense policies lock in costs today, shielding against future price increases.

- Supplemental coverage: Many combine senior life insurance with existing policies or use it where term life has expired.

For those with health conditions common in later years, guaranteed issue life insurance for seniors ensures acceptance without invasive exams or lengthy underwriting.

Types of Senior Life Insurance Plans Available in 2026

Seniors have several practical options designed for their needs and health realities.

Guaranteed Issue Whole Life Insurance

These policies require no medical exam and no health questions—acceptance is guaranteed within age limits (typically 45–85). Coverage is modest ($2,000–$25,000 or up to $30,000 with some carriers like AARP/New York Life). They feature a 2-year graded benefit period: full payout for accidental death from day one, but only return of premiums plus interest (10–30%) for natural causes in the first two years. Premiums are fixed and higher due to guaranteed acceptance. Ideal for those with serious health issues.

Simplified Issue Life Insurance

You answer a few health questions but skip the medical exam. Approval is faster than fully underwritten policies, with higher coverage possible ($10,000–$100,000+). Immediate full death benefit for most natural causes if approved. Better rates than guaranteed issue for those in average or better health.

No Medical Exam Life Insurance for Seniors

Many carriers offer accelerated underwriting or fully no-exam options via phone or online applications. These blend simplified questions with instant decisions for eligible applicants. Coverage can reach higher limits than guaranteed issue, with immediate benefits in many cases.

Term Life (for Younger Seniors)

Available for healthier seniors in their 50s–70s (up to age 80 in some cases). Provides coverage for a set period (10–30 years) at lower premiums. Best if you need temporary protection or have a mortgage/ debts to cover. Convertible to permanent in many policies.

Final Expense / Burial Insurance

Small whole life policies ($5,000–$50,000 typically) designed specifically for funerals, cremation, and related costs. Most are simplified or guaranteed issue, with fixed premiums and lifetime coverage. Often called burial insurance 2026, these pay quickly to beneficiaries—usually within days.

Best Senior Life Insurance Plans in 2026

“Best” depends on your age, health, budget, and coverage needs. Here are standout categories based on 2026 industry data, carrier strength, and beneficiary feedback.

Best Overall Senior Life Insurance Plans

Mutual of Omaha and State Farm frequently rank highly for their balance of affordability, reliability, and options. Mutual of Omaha excels in final expense and no-exam whole life up to age 85, with competitive rates and strong customer service. State Farm offers flexibility, including policies up to age 90 in some lines, and is praised for agent support. Pacific Life stands out for term and permanent options with favorable pricing stability.

Best Guaranteed Issue Plans (No Health Questions)

- Mutual of Omaha Guaranteed Whole Life: Ages 45–85 (50–75 in NY), $2,000–$25,000 coverage.

- AARP Guaranteed Acceptance (underwritten by New York Life): Up to $30,000 for members.

- Gerber Life and Colonial Penn also offer accessible guaranteed issue, though unit-based pricing (e.g., Colonial Penn’s $9.95 plans) requires careful review of actual death benefit.

These provide true peace of mind for those declined elsewhere.

Best for Low Monthly Premiums

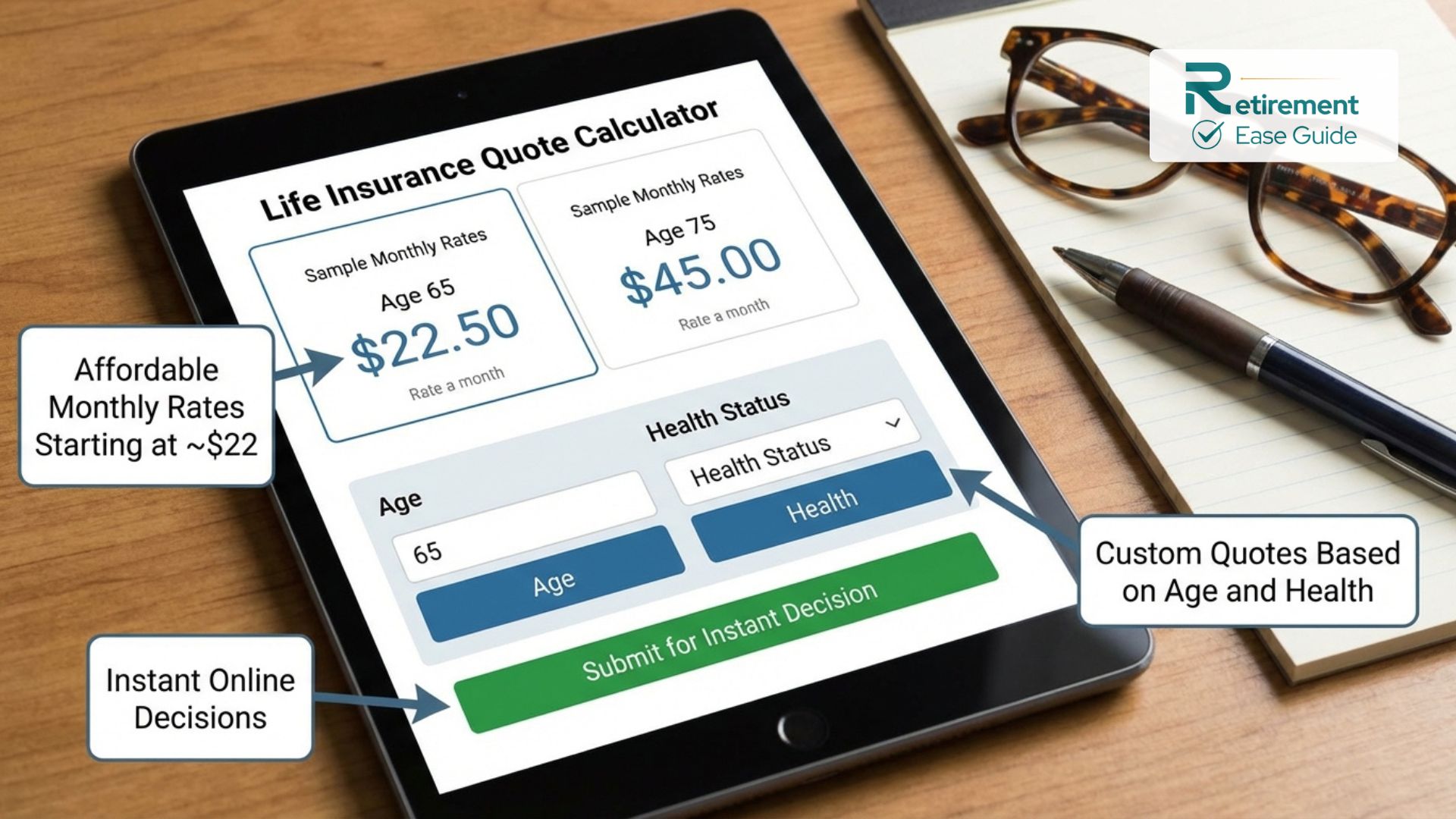

For budget-conscious seniors, look at simplified-issue final expense from Mutual of Omaha, Aetna, or Physicians Mutual. Sample rates for $10,000 coverage (non-tobacco, approximate 2026 figures):

- Age 65 female: ~$22–$42/month

- Age 65 male: ~$29–$54/month

- Age 75 female: ~$37–$72/month

- Age 75 male: ~$50–$97/month

Carriers like Penn Mutual and Banner Life often deliver strong value in term or simplified whole life for healthier applicants.

Best for High Coverage Amounts

Healthier seniors may qualify for simplified or fully underwritten whole life/universal life from New York Life, MassMutual, or Guardian, with higher limits and potential cash value growth. Term options from Pacific Life or John Hancock can provide larger temporary coverage at lower cost.

Best for Ages 50–85

Most carriers target this range. Mutual of Omaha and USAA shine for broader availability and no-exam options into the mid-80s. For ages 80+, guaranteed or simplified final expense from Mutual of Omaha or similar remains practical, though premiums rise.

Top Insurance Companies for Seniors in 2026

Here’s an expert overview of leading carriers:

- Mutual of Omaha: Strong in final expense and guaranteed/simplified whole life. Pros: Competitive rates, high issue ages (to 85), reliable claims. Cons: Guaranteed issue has 2-year graded period. Excellent for no medical exam life insurance for seniors.

- AARP / New York Life: Trusted name with guaranteed acceptance up to $30,000. Pros: Member benefits, financial strength of New York Life. Cons: Limited max coverage in guaranteed plans.

- State Farm: Local agents provide personalized service. Pros: Policies to age 90, strong ratings. Cons: May require more underwriting for higher coverage.

- Gerber Life: Affordable guaranteed options, especially known for accessibility. Pros: Simple for families. Cons: Modest coverage limits.

- Colonial Penn: Famous for TV advertising and unit pricing. Pros: Easy guaranteed issue. Cons: Often more expensive per benefit dollar—review actual payout carefully.

- Pacific Life: Competitive for term and permanent. Pros: Affordable rates, stability. Good for healthier seniors seeking value.

- Others worth considering: MassMutual (cash value growth), Guardian (dividends), Aetna (final expense options).

Always compare based on your ZIP code, health, and needs—rates vary.

Side-by-Side Comparison Table of Top Senior Life Insurance Plans

The table below shows representative 2026 sample monthly premiums for $10,000 final expense / burial coverage (non-tobacco, level benefit where applicable). Actual quotes depend on health, location, and exact product. Guaranteed issue includes 2-year graded period.

| Carrier / Plan Example | Underwriting Type | Ages Available | Sample Age 65 Premium (F/M) | Sample Age 75 Premium (F/M) | Key Features | Best For |

| Mutual of Omaha (Final Expense) | Simplified / Guaranteed | 45–85 | ~$22–$42 / ~$29–$54 | ~$37–$72 / ~$50–$97 | Fixed premiums, quick payout | Overall & no-exam |

| AARP / NY Life Guaranteed | Guaranteed Issue | 50–80+ | ~$25–$45 / ~$35–$60 | ~$45–$80 / ~$65–$110 | Up to $30k, member perks | Guaranteed acceptance |

| Gerber Life Guaranteed | Guaranteed Issue | 50–80 | ~$28–$48 / ~$38–$65 | ~$50–$85 / ~$70–$120 | Simple application | Accessibility & families |

| Colonial Penn (Unit-based) | Guaranteed Issue | Varies | Varies (check units) | Varies (check units) | $9.95 unit marketing, lifetime coverage | Brand familiarity |

| Physicians Mutual / Aetna options | Simplified | To 85 | ~$20–$40 / ~$28–$52 | ~$35–$70 / ~$48–$92 | Affordable final expense | Low premiums |

| Pacific Life (Term or Perm) | Simplified / Underwritten | To 80–90 | Lower for term if healthy | Higher for older ages | Competitive rates, convertibility | Healthier seniors & value |

| State Farm Whole Life | Varies | To 90 | Competitive agent quotes | Competitive agent quotes | Personalized service, strong ratings | Agent-supported planning |

Rates are illustrative averages synthesized from 2026 industry data and sample quotes. Get personalized quotes for accuracy.

How to Choose the Best Senior Life Insurance Plan in 2026?

Follow this expert checklist:

- Determine coverage amount: Aim for $10,000–$25,000+ to cover funerals plus extras (debts, taxes).

- Assess premium affordability: Ensure it fits your fixed income—premiums should never increase in whole life/final expense.

- Evaluate waiting periods: Guaranteed issue has 2 years graded; simplified often offers immediate coverage.

- Consider cash value: Whole life builds tax-deferred savings you can access if needed.

- Payout speed and claims process: Reputable carriers pay beneficiaries quickly.

- Health and underwriting: Answer questions honestly; guaranteed issue if health is a barrier.

- Company financial strength and ratings: Look for A or A+ from AM Best.

[Internal link placeholder: Compare with Medicare options in retirement planning.]

Shop multiple carriers—small differences in rates or benefits add up.

Common Mistakes Seniors Make When Buying Life Insurance

- Choosing the cheapest advertised premium without checking actual death benefit (e.g., unit pricing).

- Delaying purchase—rates rise with age and health changes.

- Overlooking the graded period in guaranteed issue.

- Not reviewing the policy’s fine print on exclusions or contestability.

- Buying without comparing quotes from at least 3–4 carriers.

- Focusing only on premium instead of total value and beneficiary needs.

Conclusion

Best senior life insurance plans in 2026 offer practical, compassionate protection tailored to your stage of life. From affordable senior life insurance plans and final expense insurance 2026 to guaranteed issue and no medical exam options, you can secure coverage that fits your health, budget, and peace-of-mind goals. Acting sooner locks in lower rates and ensures your family is protected without added stress during difficult times.

Selecting the right senior life insurance plan in 2026 is one of the most important financial decisions you can make for your family’s peace of mind. Don’t leave your loved ones burdened with final expenses. Our licensed insurance specialists have helped thousands of seniors secure affordable, reliable coverage with minimal hassle. Get your free, personalized senior life insurance quote and expert guidance today. Click here to speak with a senior life insurance specialist now.

Frequently Asked Questions (FAQ)

What are the best senior life insurance plans in 2026?

Mutual of Omaha, State Farm, and AARP/New York Life often rank highly for accessibility, rates, and reliability.

How much does final expense insurance cost in 2026?

For $10,000 coverage, expect $20–$60/month at age 65 and $35–$110/month at age 75, depending on gender, health, and carrier.

Is guaranteed issue life insurance for seniors worth it?

Yes, if health conditions prevent other coverage—it guarantees acceptance, though with a graded benefit period.

Do no medical exam life insurance policies for seniors have waiting periods?

Simplified issue often provides immediate full coverage; guaranteed issue typically has a 2-year graded period.

What is the difference between burial insurance and regular life insurance?

Burial/final expense is smaller whole life focused on end-of-life costs, while traditional life insurance may offer higher coverage or cash value.

Can seniors over 80 get life insurance in 2026?

Yes—many final expense and guaranteed issue options extend to 85. Coverage amounts and premiums are higher.

Does senior whole life insurance build cash value?

Yes, permanent policies accumulate cash value over time that grows tax-deferred.

How quickly do burial insurance benefits pay out?

Most reputable carriers process claims within days to a couple of weeks once documentation is provided.